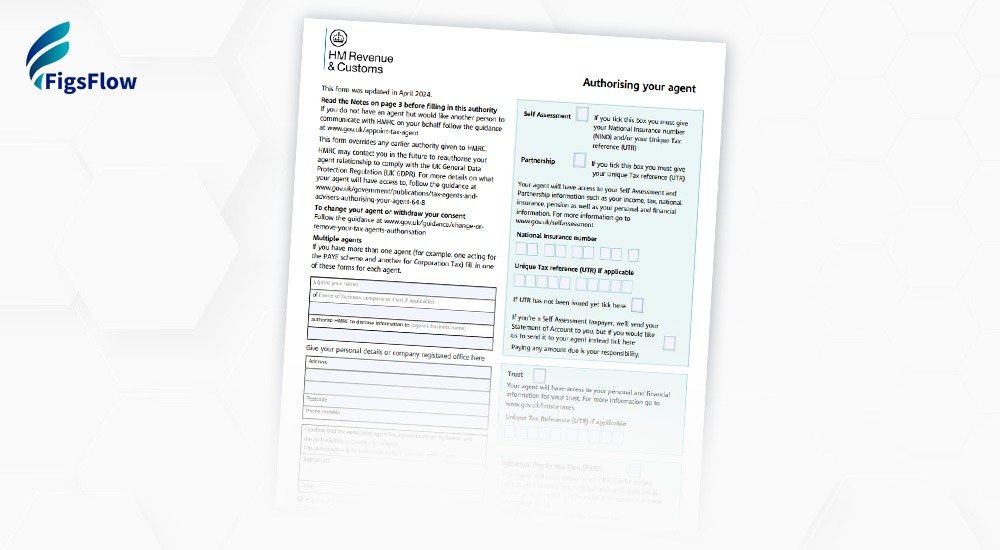

Essential Guidelines When Completing the Form

- Use the Correct Version – Ensure you are using the ‘Authorising your agent (64-8)’ version of the form. This is the specific version designed for authorisation purposes.

- Agent Code or Reference Number – Your client must enter your relevant agent code or reference number in the designated field. For example, in the ‘Agent code (SA)’ box, include the correct six-character code (e.g., 1111XX) for Self Assessment. Similar precise codes apply for other tax regimes, such as PAYE or VAT.

- Clarity & Accuracy – All information on the form must be typed or written clearly. Do not include additional comments or extraneous information in the form fields stick strictly to the requested data.

- No Extra Notations – Avoid adding a covering letter unless it contains essential information required to process the form. Any crucial details must be included on the form itself; do not write in the margins or add stray notes.

- Specific Instructions for CIS – If the authorisation includes the Construction Industry Scheme (CIS) for contractors, your client should clearly note this on the form or attach a separate letter. This ensures that HMRC recognises the additional scope of the authorisation.

Special Considerations for Different Tax Matters

- Tax Credits – For tax credits, your client must complete a form 64-8—there is no option to set up this authorisation online. Additionally, if the claim involves joint tax credits, both claimants must sign the same form.

- Personal Representatives – When dealing with the estate of a deceased person, personal representatives use form 64-8 to authorise you to manage individual PAYE, Self Assessment, or National Insurance affairs. The person completing the form must include:

- Their signature, name, and address.

- The deceased person’s National Insurance number or Unique Taxpayer Reference (UTR) in the appropriate section.

- Corporation Tax – If the authorisation is exclusively for Corporation Tax, send the form to the HMRC office responsible for Corporation Tax.

- High Net Worth Unit – If HMRC’s High Net Worth Unit deals with your client’s affairs, direct the form to that unit.

- Charity Matters – For charities, send the completed form to the Charities Correspondence Team.

- Trusts – For authorisations regarding a trust’s tax affairs, the form should be sent to the Trusts and Estates Team.

- R40 Form Repayment Claims – If the authorisation accompanies a claim for a R40 form repayment, send the form along with the claim to HMRC.

By following these specific submission instructions, you help ensure that HMRC can process the authorisation quickly and accurately.

Maintaining Compliance: What Being Authorised Does & Doesn’t Mean

It is important to understand that while being authorised as an agent enables you to act on behalf of your client with HMRC, it does not transfer any of the client’s legal obligations to you. You are still acting as their agent, which means:

- Client Responsibilities Remain – The ultimate responsibility for the tax affairs lies with your client. Your role is to assist and manage communications, but the legal liabilities remain theirs.

- Ongoing Communication – Even after authorisation, HMRC will continue to write to your client regarding certain tax matters, such as tax credits. However, you are also empowered to deal with HMRC directly in writing or via telephone.

- Record Keeping – It is crucial to maintain accurate records of all authorisations and communications. This not only helps in managing your client’s tax affairs but also ensures that you can provide evidence of authorisation if required.

Best Practices for a Smooth Authorisation Process

To minimise delays and avoid common pitfalls, here are several best practices for managing the authorisation process with form 64-8:

- Review Before Submission – Encourage your clients to double-check all information on the form before sending it to HMRC. Even minor errors can lead to processing delays.

- Clear Communication – Provide your clients with clear, step-by-step instructions on how to complete the form. This includes explaining where to enter your agent code and the importance of writing legibly.

- Timely Submission – Remind clients of the importance of sending the form to the correct HMRC office. If your client is unsure which office to use, consult HMRC’s latest guidance or reach out for clarification.

- Follow-Up – Once the form has been sent, follow up with HMRC if you do not receive confirmation of authorisation within the expected timeframe. This proactive approach helps ensure that any issues are resolved promptly.

- Digital Alternatives Where Possible – Although form 64-8 is widely used, if an online authorisation option is available for a particular tax service, consider encouraging your client to use the digital route. This is often faster and more secure.

Conclusion

Formal authorisation through form 64-8 is a critical process for tax agents and advisers. It provides the necessary legal framework that allows you to interact with HMRC on your client’s behalf while ensuring that all parties’ rights and responsibilities are clearly defined. Whether dealing with individual tax affairs, Corporation Tax, PAYE, or specialised areas like the Construction Industry Scheme, correctly completing and submitting form 64-8 is essential for maintaining compliance and ensuring efficient communication with HMRC.

By adhering to the detailed guidelines provided above—such as entering the correct agent codes, avoiding extraneous information, and sending the completed form to the appropriate HMRC office—you help safeguard both your client’s interests and your own professional standing. Remember, while authorisation enables you to act as an intermediary, the client’s legal obligations remain their responsibility.