CPA Engagement Letters: The Clauses, Samples & Risk Protection Every Firm Needs

A CPA engagement letter defines scope, fees and liability — your firm's first defense against malpractice claims. See the must-have clauses and a free sample.

A CPA engagement letter is a written contract between a CPA firm and a client that defines the scope of services, fees, responsibilities, and liability limits before work begins. Issued by a licensed CPA, it is governed by AICPA standards and, for tax work, Circular 230. It is your firm’s first defense in a fee, scope, or malpractice dispute. A handshake and a verbal scope do not hold up when a client disputes a fee or a filing goes sideways. A CPA engagement letter does.

An engagement letter is your firm’s first line of defense, not its filing formality. This guide breaks down what the letter has to contain, the clauses that carry the legal weight, how confidentiality actually works, and where firms leave themselves exposed.

What Is a CPA Engagement Letter?

An engagement letter is a written contract between a professional firm and a client that sets out the work the firm will do, the fees it will charge, and the responsibilities each side carries. It turns a verbal understanding into enforceable terms before any work begins. Most professions that deliver defined services under a fee use one.

A CPA engagement letter is a written contract issued by a Certified Public Accountant or a CPA firm. What sets it apart is the authority behind it and the standards it answers to. It comes from a licensed professional bound by AICPA standards and, for tax work, by Circular 230, which shapes the scope language, the confidentiality terms, and the way liability is framed inside the letter.

The letter applies across every service line a CPA offers, including tax preparation, bookkeeping, compilations, reviews, audits, and advisory work. Each engagement type carries different risks, so the letter is tailored to the scope rather than issued as one generic form.

Who Needs a CPA Engagement Letter?

Any CPA or CPA firm delivering paid services should issue a CPA engagement letter, whatever the engagement size. Solo practitioners need one as much as large firms, because the letter – not the firm’s size – is what defines scope and caps liability. A CPA engagement letter is worth issuing even for a small, one-off engagement, since a modest job can still generate a claim larger than its fee.

What a CPA Engagement Letter Actually Protects You From

When a firm skips the engagement letter, the cost tends to surface in three areas. Fees become harder to recover, the scope of work is more open to dispute, and the firm carries malpractice exposure it could otherwise have limited.

It helps to look at each in turn. Where no signed scope exists, a client may argue you agreed to work you never actually quoted, and without something in writing that is a difficult claim to answer. Where the letter says nothing about fees, recovering an unpaid bill can come down to your account of the arrangement against the client’s. And where there is no limitation of liability, a single dissatisfied client may be able to pursue damages well beyond the fee the engagement ever earned.

A well drafted engagement letter tends to close each of these gaps. It records the scope in writing, so both sides share the same understanding of what was agreed. It sets out payment terms that a court is able to enforce. And it places a ceiling on how much the firm can be held liable for, wherever state law allows one.

This is part of why professional liability carriers usually ask to see the engagement letter once a claim arises. As a rule, the firms that issue one on every engagement are also the firms best placed to defend a claim when it comes.In short, the CPA engagement letter is the document that turns a dispute from your word against the client’s into a written record a court can read.

Risk callout

A letter the client has not signed is not yet a contract. If work begins before the signature comes back, the firm carries the full risk of the engagement with none of the protection.

What Every CPA Engagement Letter Should Include

Before any work starts, a strong engagement letter settles four questions. What will the firm actually do, what will it cost, who is responsible for what, and what happens if the relationship ends. Almost every clause in the letter exists to answer one of those four, and everything else is detail that hangs off them.

A few clauses do most of the real work here. They are the ones that get tested when a client pushes back or a claim comes in, so they are worth understanding one at a time.

Parties & Effective Date

This names who the agreement is between and when it starts. It identifies the firm, the client, any entity the client files or trades through, and the date the terms take effect. On a joint matter, both individuals are the client and both sign. Getting the correct legal names down removes any later doubt over who owes the fee and who is authorized to approve the work.

Scope of Services

This is where most disputes are either prevented or created. The clause states the exact services the firm is taking on and ties them to the period they cover. Written loosely, a single line like “accounting services” invites the client to read in everything they happen to need. Written tightly, it fixes the boundary the rest of the letter depends on.

Services Not Included

Naming what the firm will do only draws half the line. The other half is stating plainly what it will not do, and that half is where most arguments begin. Clients tend to bundle preparation, planning, bookkeeping, and representation together as one service and assume all of it comes with the fee. Spelling out the common exclusions in advance keeps a later request from being mistaken for a broken promise.

Client Responsibilities

This sets out what the client must provide and by when, including the records, information, and access the firm relies on to do the work. Because so much of a CPA’s output depends on client-supplied data, the clause quietly shifts the risk of late or inaccurate information back to the party who controls it. It also confirms that the firm works from what the client represents rather than independently verifying every figure.

Fees & Payment Terms

This turns the money conversation into a written term. It records the fee, how and when the client will be billed, the rate for anything outside the agreed scope, and when payment is due. Where the firm holds delivery until the invoice is settled, that belongs here too. When a bill later goes unpaid, this is the clause that decides whether recovery rests on a documented arrangement or on competing memories.

Timelines & Deadlines

Much CPA work runs on a fixed calendar, and the letter should run on it too. This clause sets the deadline for the work and, just as importantly, the date by which the firm needs complete information to meet it. Tying the delivery date to the client’s cooperation rather than the firm’s capacity keeps a late document drop from becoming the firm’s missed deadline.

Confidentiality & Data Security

CPAs handle some of the most sensitive information a client holds, and this clause states how the firm protects it. It commits the firm to reasonable safeguards and can note where the data actually lives, such as secure portals, third-party software, and e-signature tools, along with the client’s own duty to keep credentials safe. It documents a professional obligation, though as covered later, it does not by itself create legal privilege.

Termination

This sets the exit terms before anyone needs them. It describes how either side can end the engagement, how much notice is required, how the final bill is settled, and how the client’s records are returned. A clear exit route gives the firm a professional way to step away from a relationship that has stopped working, rather than being locked into it.

Limitation of Liability

This marks the outer edge of the firm’s responsibility, to the extent state law allows, and because it carries real legal consequences an attorney should review it before use. Broadly, it can confirm that the firm is not answerable for errors tracing to incomplete, inaccurate, or late client information, and that decisions on the client’s own affairs remain the client’s. Without such a clause, a modest engagement can carry exposure many times larger than the fee, which is why it matters most in audit and attest work.

Not every clause carries the same weight in every engagement. Limitation of liability does the most work in audit and attest engagements, while client responsibilities matters most wherever the firm relies on records the client supplies, which is very nearly everywhere.

Together, these nine clauses are what make a CPA engagement letter enforceable rather than merely a formality.

| Clause | What it does | Why it matters |

|---|---|---|

| Parties and effective date | Names the firm, the client, any entity involved, and the start date | Removes doubt over who owes the fee and who can approve the work |

| Scope of services | States the exact services covered and the period they cover | Prevents a loose line like “accounting services” from expanding on its own |

| Services not included | Names the work the firm is not taking on | Stops a later request from being mistaken for a broken promise |

| Client responsibilities | Sets out the records and information the client must provide, and by when | Shifts the risk of late or inaccurate data back to the client |

| Fees and payment terms | Records the fee, billing schedule, out-of-scope rate, and payment due dates | Makes an unpaid bill an enforceable term rather than a memory contest |

| Timelines and deadlines | Fixes the delivery deadline and the information cutoff to meet it | Ties the deadline to client cooperation, not the firm's capacity |

| Confidentiality and data security | Commits the firm to safeguarding client information | Documents a professional duty and sets expectations for how data is handled |

| Termination | Sets how either side exits, the notice required, and how records return | Provides a clean way out of a relationship that has stopped working |

| Limitation of liability | Caps the firm's exposure, where state law allows | Keeps a modest engagement from carrying outsized liability |

Where Firms Get Engagement Letters Wrong

The problem is rarely that a firm has no letter at all. Most firms have one. The trouble is that the letter on file no longer matches the work actually being done, and a letter that describes the wrong engagement offers very little protection when a dispute arrives.

Four patterns cause most of the trouble.

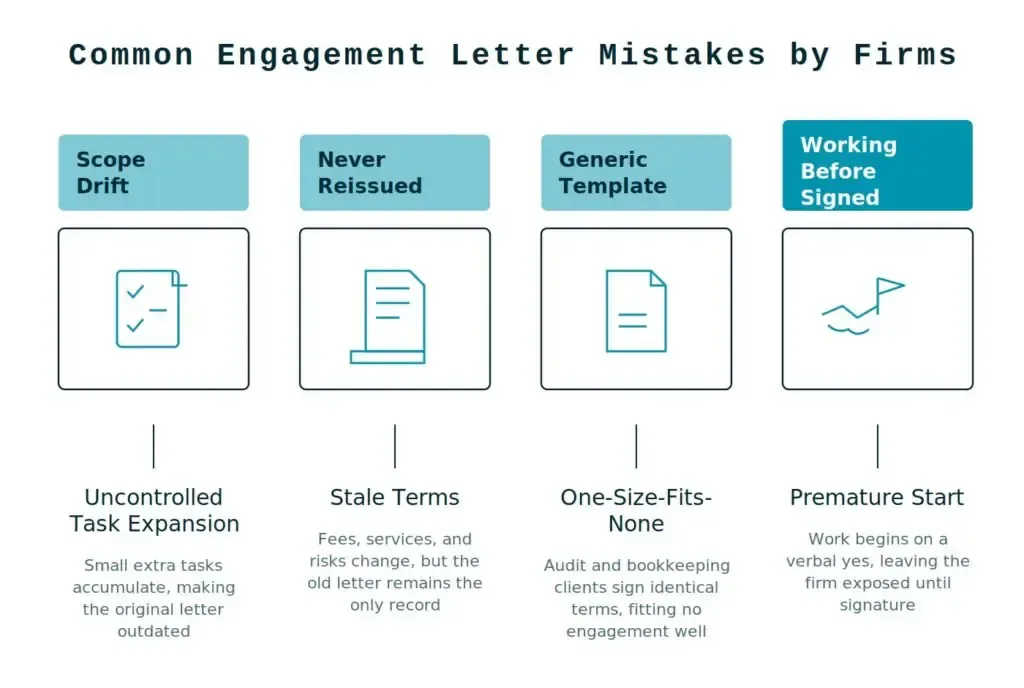

Scope Drift

An engagement usually starts inside its stated boundaries, then slowly widens. A client asks for one small extra task, then another, and the firm obliges without updating the letter. Months later the work bears little resemblance to what was signed, and if a disagreement surfaces over one of those added tasks, the letter is silent on exactly the point in question.

A Letter That Is Never Reissued

A firm signs a client once and treats that letter as permanent. Meanwhile the services grow, the fees change, and the risks shift, yet a document signed three years ago still stands as the only written record. When it matters most, the firm is relying on terms that describe a relationship that no longer exists.

One Generic Template for Every Service Line

A single all-purpose letter feels efficient, but it forces very different engagements into the same wording. An audit client and a bookkeeping client sign identical terms, so the limitation of liability that an audit needs sits alongside scope language that fits neither. The result is a letter that technically exists but protects no engagement well.

Working Before the Letter Is Signed

With a deadline approaching, it can be tempting to begin once the client agrees on a call, even though the signed letter has not yet come back. In that window, there is really only a verbal understanding in place rather than a contract. If everything goes smoothly, this tends to go unnoticed. If a problem comes up before the client has signed, though, the firm may find it has taken on the risk of the work without the protection the letter was meant to provide.

CPA Engagement Letter Samples by Service Type

A sample only helps if it fits the engagement in front of you. A tax preparation letter and a bookkeeping letter are built on the same core clauses, but they differ in how the scope is written, what the firm delivers, and which client responsibilities carry the most risk.

Below are two service-specific guides, each with a template you can adapt.

- Bookkeeping engagement letters — covers recurring scope, monthly boundaries, and the record-quality terms that protect a bookkeeping firm. Read the bookkeeping engagement letter guide →

- Tax preparation engagement letters — covers filing-season scope, the rule of signing before any work starts, and Circular 230 points to keep in mind. Read the tax preparation engagement letter guide →

Pick the template closest to your engagement, then adjust the scope and fees to suit the client you are working with.

Standardizing Engagement Letters Across Your Firm

Knowing what a strong letter contains is one problem. Getting every letter your firm sends to hit that standard, every time, is a different one.

Manual drafting is where the standard slips. Templates live on individual desktops, wording drifts partner to partner, letters go out unsigned, and no one can say which version a given client actually holds. The larger the firm, the wider the drift.

This is the gap FigsFlow closes. Figsflow gives firms customizable CPA engagement letter templates, an automated workflow for drafting, reviewing, and finalizing each letter, and secure cloud storage so every signed letter sits in one place. Standardizing every CPA engagement letter across the firm is exactly the problem FigsFlow was built to solve. Letters go out with consistent terms, get sent and e-signed digitally, and are tracked centrally, so a partner can see at a glance which letters are drafted, sent, and signed. The standard stops depending on who drafted the letter.

Conclusion

Scope it precisely, sign it before the work starts, and reissue it every year. That sequence is the whole discipline.

A firm that follows it defends fee disputes, blocks scope creep, and hands its liability carrier a clean file after a claim. A firm that skips it carries every engagement’s risk on a document that no longer describes the work.

Before your next engagement goes out, ask, does this letter match the work I am about to do, and has the client signed it yet?