A tax preparation engagement letter is what settles that. It is a written record of what you agreed to do, so you can point to the terms you both accepted. A tax preparation engagement letter is a written agreement between a tax preparer and a client that defines which returns and tax year the preparer will handle, the fee, the information the client must supply, and where the preparer’s responsibility ends.

The stakes are real. Of the claims filed in 2023 against firms in the AICPA Professional Liability Insurance Program, roughly 75% came from tax services, and more than half of those had no tax preparation engagement letter on file (The Tax Adviser, citing CNA).

Here is what a tax preparation engagement letter should contain, the clauses that hold up when a client pushes back, a free template you can adapt, and a checklist for getting every letter signed before intake opens.

What Is a Tax Preparation Engagement Letter?

A tax preparation engagement letter is a written agreement between a tax preparer and a client that sets out the returns you will prepare, the fee, the information the client must supply, and the point at which your responsibility ends.

The letter names the tax year and the specific returns in scope, so “do my taxes” does not quietly expand into bookkeeping, planning, or audit defense. For the client, it confirms what they are paying for and what they have to hand over to keep the work moving.

A signed letter can act as a binding contract, and it records what you agreed to do, which matters when the IRS examines a return and the client asks why a position was taken.

Who Needs a Tax Preparation Engagement Letter?

Any preparer who files returns for a fee should issue a tax preparation engagement letter — CPAs, EAs, and unenrolled preparers alike. A solo preparer needs a tax preparation engagement letter as much as a large firm does, because the letter, not the firm’s size, is what fixes scope and limits liability when a return is questioned.

Why Tax Firms Need an Engagement Letter

A tax preparation engagement letter fixes the scope of work in writing. When a client asks for something outside it, you have a document to point to rather than an awkward conversation to improvise.

It settles money before money becomes a dispute. Flat fee or hourly, what the out-of-scope rate is, when payment is due, whether the return gets filed before or after you are paid.

In short, a tax preparation engagement letter helps your firm:

- Define the exact returns and schedules covered, so “tax prep” is not left to interpretation

- Contain scope creep, because work you did not name is work you did not agree to do

- Set out client responsibilities, including complete records delivered on time

- Fix payment terms, including due dates and the rate for anything extra

- Document the limits of your responsibility for a professional liability claim

- Standardize onboarding, so every client starts the season the same way

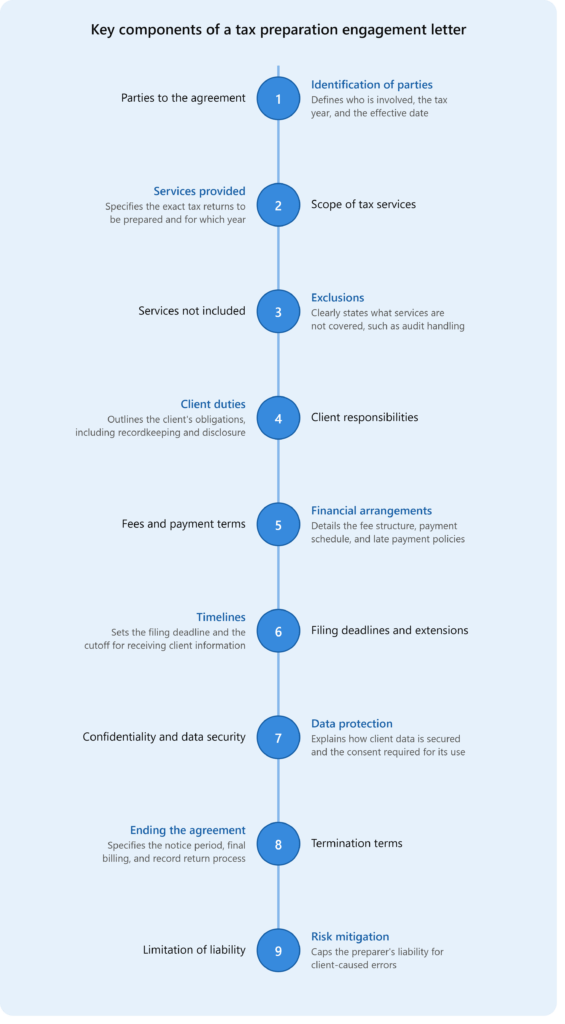

What Should a Tax Preparation Engagement Letter Include?

A good tax preparation engagement letter covers what it needs to without running long, and stays clear enough that the client actually reads it. It should settle four things. Which returns you will prepare, which you will not, what the client has to give you, and how the work moves from signed letter to filed return.

These are the sections every tax preparation engagement letter should carry.

Parties to the Agreement

Name who the agreement is between and when it takes effect.

This usually covers:

- The name of the tax firm or preparer

- The client’s name, and both names if the return is joint

- The client’s business or entity name, where relevant

- The tax year the engagement covers

- The effective date

Where the client files through an entity, use the correct legal name. It removes any doubt over who owes the fee and who is authorized to approve the return. On a joint return, both spouses are the client, and both sign.

For example,“This letter confirms the terms under which [Firm] will prepare the 2025 federal and state income tax returns for [Client].”

Scope of Tax Services

Scope is the most important section of a tax preparation engagement letter, because it defines the work everything else depends on. It states exactly which returns you will prepare and for which year.

Be specific about this. If you only write “tax preparation,” the client is free to assume it covers every form and situation they have, and they usually will. List the exact returns instead.

For example,preparation of the federal Form 1040 and the schedules that apply, one resident-state return, and a review of the prior-year return for carryforward items. If the client has rental property, a K-1, or a second state, name those or price them separately.

Name the specific tax year and cover only that year. This keeps the engagement from rolling forward into future returns you never agreed to prepare, and it sets a clear limit on the due diligence Circular 230 Section 10.22 requires of you. Say when your work ends too, either when you hand the finished return to the client to file, or when you file it on their authorization.

Services Not Included

Listing what you will do only draws half the line. The other half is stating what you will not do, and that half is where most arguments begin.

Clients tend to lump preparation, planning, bookkeeping, and IRS representation together as one service. Unless you say otherwise, they will expect all of it for the fee they paid. So name the common exclusions plainly

Of all these exclusions, audit and notice handling is the one to be most explicit about. If the IRS examines the return or sends a notice after filing, that is a new engagement with its own letter and its own fee. Make that clear in advance, not once the notice has already landed on the client’s desk.

Client Responsibilities

A return depends on what the client gives you. The responsibilities section makes that dependency explicit.

The client is typically responsible for:

- Providing complete and accurate records

- Delivering W-2s, 1099s, K-1s, receipts, and basis information

- Disclosing all income, including foreign accounts and foreign income

- Responding to questions promptly

- Reviewing the return before it is filed

- Signing Form 8879 to authorize electronic filing, and approving any extension

One point matters most here. You prepare the return from what the client gives you. You do not audit or verify it independently. Circular 230 lets you rely in good faith on their information, but you must ask questions when something looks wrong or incomplete. The letter should state that you rely on what they provide and will follow up when something does not add up.

Fees & Payment Terms

If the fee is unclear now, it becomes a payment dispute later. State the fee plainly.

- Flat fee, hourly rate, or a base fee plus hourly for complications

- Any minimum or deposit due before work begins

- The rate for out-of-scope work

- When payment is due

- Late-payment terms

If you charge a flat fee, say what it covers, which return, which schedules, one state. If added work is billed hourly, state the rate and when it kicks in. A common and defensible approach is to require written approval before any out-of-scope work starts.

Many firms hold filing until the fee is paid. If that is your policy, put it in writing, so the return will not be e-filed until the invoice is settled.

Filing Deadlines & Extensions

Tax work runs on a hard calendar, and the letter should run on it too.

Set the filing deadline and, critically, the date by which you need complete information to hit it. If the documents arrive after that cutoff, the letter should say in advance that an extension may be necessary.

Warning

An extension only gives the client more time to file the return. It does not give them more time to pay. Any tax owed is still due by the original deadline, and anything unpaid after that keeps building penalties and interest. Make sure the client understands this, so they do not treat an extension as extra time to pay.

For example , “To file your return by April 15, 2026, we must receive your complete information by April 1, 2026. Information received after that date may require an extension.” State that filing an extension needs the client’s express approval, and that you will base it on the information available at the time.

Confidentiality & Data Security

Tax preparers handle some of the most sensitive data a client has. The letter should address how you protect it.

State that your firm takes reasonable steps to safeguard client information and handles records securely. It is also worth noting where the data lives:

- Secure client portals for document exchange

- Third-party tax software and e-file transmitters

- E-signature platforms

- The client’s own responsibility to keep login credentials secure

One US-specific obligation sits here. Under IRC Section 7216, a preparer generally must obtain the client’s written, signed consent before using or disclosing their tax return information for anything beyond preparing the return itself, including cross-selling other services. If your engagement might involve that, the consent belongs in your process, and the letter is a natural place to flag it.

Termination Terms

Set the exit terms before you need them. Without them, a client can walk away mid-engagement and then argue over the fee for work you already did.

Cover four things. How either side ends the engagement, how much notice is needed, how the final bill is settled, and how records are returned. One rule to know here is that Circular 230 Section 10.28 requires you to return the client’s own records promptly when they ask, even during a fee dispute. You may keep copies, and you may hold back work you prepared yourself where the rules allow it.

For example, either party may end the engagement with 30 days’ written notice, the client pays for all work completed up to that date, and their records are returned promptly.

Limitation of Liability

This section sets the outer edge of your responsibility, and because it carries legal consequences, an attorney should review it before you use it.

Broadly, it can clarify that you are not responsible for errors that trace to incomplete, inaccurate, or late information from the client, and that positions on the return rest on what the client represented. It can also confirm that decisions about the client’s tax positions and business affairs remain the client’s.

For example, you prepare the return from the figures the client provides. If those figures are wrong, the resulting return is not your liability. Depending on state law and your professional guidance, this section may also cap the type or amount of damages your firm can be exposed to.

Free Tax Preparation Engagement Letter Template

The sample below is a short illustration. Adapt it to your services, your state, and your fee structure, and have an attorney review the legal clauses before you send it to a client.

Filing-Season Engagement Letter Checklist

The letter only protects you if it is signed before you touch the return. In a compressed season, that means getting the process done early and tracking it deliberately. Run this before intake opens.

| Step | What to Do | Why It Matters |

|---|---|---|

| Refresh the letter | Update the tax year, fee, and scope language from last season | Reusing last year's letter after a fee or scope change leaves you protected on the wrong terms |

| Batch-send early | Send letters to returning clients before you accept documents | A letter chased down in March is a letter that never gets signed |

| Confirm signature first | Do not start any return until the signed letter is back | An unsigned letter protects no one, and more than half of tax-service claims involved no engagement letter |

| Handle Section 7216 consent | Collect written consent where you will use return data beyond preparation | Federal law requires it before disclosure or use |

| Set the information cutoff | State the date complete records are due to meet the deadline | Ties the filing date to client cooperation, not to your capacity |

| Track who has signed | Log signed versus outstanding letters in one place | Email and PDF folders lose letters exactly when you need them |

Common Mistakes to Avoid in a Tax Preparation Engagement Letter

A tax preparation engagement letter only works when it is specific, current, and matched to the work you are actually doing. Plenty of firms use one and still get caught out because the document is generic or stale.

- Vague scope. “Tax services as needed” hands the client a blank check to interpret, and they will read it generously

- No exclusions. Naming what you do without naming what you do not leaves half the boundary undrawn

- Planning and representation left unclear. These are the services clients most often assume come free with the return

- Undefined client responsibilities. With no dated obligations, late records become your missed deadline

- No information cutoff. Without a date, every return becomes a last-minute scramble

- Starting before the signature. The single most common gap, and the one that sinks liability claims

- Reusing last season’s letter unchanged. When the fee or scope moves, the letter has to move with it

How FigsFlow Helps With Tax Preparation Engagement Letters

Writing a strong engagement letter is only the start. During filing season you also need to send it, get it signed, and know at a glance who still has not returned it.

FigsFlow helps tax and accounting firms manage that whole process in one place.

With FigsFlow, you can build reusable engagement letter templates, tailor them for each client, send them for e-signature, and track which letters are signed and which are still outstanding, all without chasing PDFs through email.

FigsFlow can help your firm:

- Build reusable tax engagement letter templates

- Customize each letter for the client and tax year

- Send for e-signature

- Track signed and unsigned letters in one dashboard

- Batch-send to returning clients before the season starts

- Keep every client agreement organized and retrievable

- Cut the manual admin that piles up at intake

For firms running a full book of returning clients each season, that turns a scramble into a repeatable process.

Send and e-sign tax preparation engagement letters in minutes with FigsFlow.

Conclusion

A tax preparation engagement letter draws the line between what you agreed to do and everything a client might later assume you did.

Skip it, and you are defending a claim with no record of the terms. Sign it before the work starts, and the record is already made.

Refresh your tax preparation engagement letter, send it before intake opens, and get the signature before the first return.

FAQs

A written agreement between a tax preparer and a client. It sets out the returns you will prepare, the fee, the information the client must supply, and the point at which your responsibility ends. It names the tax year and specific returns, so scope cannot quietly expand into planning, bookkeeping, or audit defense.

Scope of returns and tax year, services excluded, client responsibilities, fees and payment terms, filing deadlines and extensions, confidentiality and IRC Section 7216 consent, termination terms, and a limitation of liability clause. Naming what you will not do matters as much as naming what you will.

No federal law requires one for every return. But Circular 230 §10.33 lists clear engagement terms as a best practice, some state boards expect them, and liability insurers treat them as essential, since a missing letter is what sinks most tax-service claims. Required or not, filing without one carries real risk.

Reuse the template, not last year’s signed copy. Each season, refresh the tax year, the fee, and any change in scope, then send it for a fresh signature before you start work. A letter naming the wrong year or an outdated fee protects you on terms that no longer apply.

Use the free template in this article as a starting point. Adapt it to your services, state, and fee structure, and have an attorney review the legal clauses before sending it to a client. Software like FigsFlow also lets you build reusable templates and send them for e-signature.