Two situations. A client leaves you. Or you need to leave them. Both uncomfortable. Both inevitable. And both require the same thing before you walk away: a disengagement letter.

A disengagement letter is a formal notice ending the professional relationship between an accountant and their client. It confirms what work is complete, what isn’t, who owes what, and where your liability stops.

Here’s exactly what goes in it, when to send it, and how to generate a compliant one in seconds.

What Is a Disengagement Letter?

A disengagement letter is a written notice from an accounting firm to a client formally ending their professional relationship. It documents the termination date, summarises completed work, clarifies outstanding responsibilities, addresses final billing, and confirms how records will be transferred.

It is not optional. It is not a formality. It is your primary protection the moment a client relationship ends.

Think of it this way. Your engagement letter defined what you agreed to do. Your disengagement letter defines where that agreement stops. Without it, there is no clean line. Work bleeds past the termination date. Clients assume you are still responsible. Disputes arise over who owes what and who owns what. Professional indemnity claims follow.

One letter. Written well. Sent promptly. That is the difference between a clean exit and a costly one.

Types of Disengagement Letter

Not all disengagement letters are the same. The situation determines the type, the tone, and what you include.

| Type | Who Initiates | Tone | Key Focus |

|---|---|---|---|

| Firm-initiated | You | Direct, factual | Business decision, no apology |

| Client-initiated | The client | Warmer | Proper exit documentation |

| Scope-specific | Either | Precise | What ends, what continues |

Firm-Initiated Disengagement

You are ending the relationship. The reasons vary.

- Non-payment

- Persistent non-cooperation

- Conflict of interest

A client whose conduct puts your firm at risk. A practice restructure that means you are no longer taking on certain work. Whatever the reason, you are in control of the timing and the wording. Your letter should be direct, factual, and free of apology. You made a business decision. The letter confirms it professionally.

Client-Initiated Disengagement

Your client is leaving. They have found another firm, decided to bring the work in-house, or simply moved on. In this scenario, your letter is warmer in tone but identical in substance. You still need to confirm the termination date, outstanding work, fees, and records transfer. The client’s leaving does not remove your obligation to document the exit properly.

Scope-Specific Disengagement

Sometimes, only part of the engagement ends. A client may stop using your bookkeeping service but keep you for tax. Or they may conclude a one-off project with no ongoing work to follow. A scope-specific disengagement letter ends a defined service without terminating the entire relationship. It needs to be precise about exactly what is ending and what continues.

When You Should Send a Disengagement Letter

If a client relationship is ending in any form, you need to send a disengagement letter. The sooner it is issued, the cleaner the separation.

Here are the situations that require one:

- A client formally notifies you that they are moving to another firm

- You are ending a relationship due to non-payment or persistent late payment

- A conflict of interest has emerged that makes continuing the engagement inappropriate

- A client’s conduct, whether uncooperative, dishonest, or legally questionable, has made the relationship untenable

- Your firm is restructuring and no longer offering services that a client relies on

- A fixed-term or project-based engagement has reached its natural end

- You are retiring, selling your practice, or transferring your client book to another firm

In every one of these scenarios, the disengagement letter is not a courtesy. It is a professional obligation. Both ICAEW and ACCA treat it as best practice, and failure to issue one is a common source of complaints to both bodies.

Good to Know: When does a disengagement letter actually become valid?

A disengagement letter becomes effective on the date it is issued or the date specified in the letter, not when it is signed. ICAEW is clear on this: even if a client refuses to sign or return it, the fact that the letter was sent is sufficient to uphold your firm’s position in any dispute.

A client signature adds weight and confirms receipt, but you are not waiting on it for your liability to end. State the effective date clearly in the letter and keep proof that it was sent.

When You Don't Need to Send a Disengagement Letter

You do not need a disengagement letter when there is no ambiguity about your responsibilities and no outstanding work or fees. This includes:

- A client who has gone inactive with nothing unresolved

- A service that is temporarily paused with a clear intention to resume

- A one-off engagement where the deliverable and final invoice mark a clean end

Just ask yourself: Is there any ambiguity about whether you are still responsible for this client’s affairs? If the answer is no, you do not need one.

What Happens If You Don't Send One

If you do not send a disengagement letter, your liability does not end. You remain professionally exposed to complaints, missed deadline claims, and indemnity issues until you can prove the relationship was formally closed. Without a letter, that proof does not exist.

Here is what that looks like in practice:

Your Liability Does Not Stop.

It stops on the day you can prove you communicated the end of the engagement. Without a letter, that proof does not exist.

Complaints Have Nowhere to Land But on You.

A client who later claims you missed a deadline or gave incorrect advice during a period you believed you were no longer acting has a genuine basis for complaint.

Professional Clearance Becomes Messy.

When a new accountant sends a clearance request, you need a disengagement letter on file to support the position you communicate in your response.

Your Insurer Will Ask for It.

If a claim arises, your professional indemnity insurer will want to see the letter. Without one, your position is immediately weaker.

The mess at the end is almost always a consequence of the ambiguity at the beginning. A disengagement letter is the line that separates your responsibility from your former client’s.

The AML Trap: What Your Disengagement Letter Cannot Say

If you are disengaging a client due to suspicious activity, your letter cannot reference that suspicion. It cannot hint at it, allude to it, or use any language a reasonably informed client could interpret as an indication that a report has been filed.

Here is why that matters.

Under section 333A of the Proceeds of Crime Act 2002, tipping off is a criminal offence. It occurs when you disclose to a client that a Suspicious Activity Report has been made, or that a money laundering investigation is underway, in a way that is likely to prejudice that investigation. You disengage. You state that you are no longer able to act. You do not give the real reason.

When the new accountant sends a professional clearance request, you are permitted to share relevant facts, though not to confirm a SAR was submitted. The profession uses specific coded language here. ACCA’s recommended wording signals to the incoming accountant that they should ask more questions without disclosing anything to the client.

If you are in any doubt about how to handle a SAR-related disengagement, contact your professional body’s ethics helpline before you send anything. Getting this wrong is not a paperwork error. It is a criminal offence.

What Every Disengagement Letter Must Include

Regardless of the type or the circumstances, every disengagement letter needs to cover the same ground. Here is what that looks like.

Effective Date

The exact date on which your services end. Not “shortly” or “at the end of the month.” A specific date. This is the line your liability stops at.

Scope of Disengagement

Which services are ending? If it is everything, say so. If it is specific services only, name them. Ambiguity here is where disputes begin.

Summary of Completed Work

What have you done up to the termination date? Brief, factual, and referenced to the original engagement terms.

Outstanding Work

What remains incomplete, and who is now responsible for it. If you will complete certain tasks before the termination date, say so explicitly. If you will not, say that too.

Final Billing

Outstanding fees, payment deadline, and how to settle. A vague reference to “amounts outstanding” creates room for dispute.

Records Transfer

How and when you will return or transfer the client’s documents. Non-payment of fees is not a legitimate reason to withhold client records. Fee disputes are a separate matter pursued through separate channels.

Liability Disclaimer

A clear statement that your firm accepts no responsibility for matters arising after the termination date.

Confidentiality Reminder

Both parties retain confidentiality obligations after the relationship ends. Saying so in writing reinforces that and protects you.

Confirmation of Receipt

Ask the client to acknowledge receipt. This is your evidence that they received and understood the notice.

Disengagement Letter Templates

Whether you are ending a relationship with a sole trader, a limited company, or a long-standing client, the letter needs to be right. A missed clause or a vague termination date is all it takes to leave your firm exposed.

The template below is built for UK accountants and covers every required section: effective date, services ending, outstanding work, final billing, records transfer, HMRC notification, and client acknowledgement. Download it, add your firm details, and it is ready to send.

How to Create a Disengagement Letter Fast

There are three ways to create a disengagement letter. You can write one from scratch or adapt a template like the one provided earlier in this guide. You can feed the full context into an AI tool like ChatGPT and have it draft one for you. Or you can use a specialised tool like FigsFlow, which generates a fully compliant, client-specific letter in seconds. Each approach works, but they are not equal.

Let’s take a look at how FigsFlow helps you craft a disengagement letter.

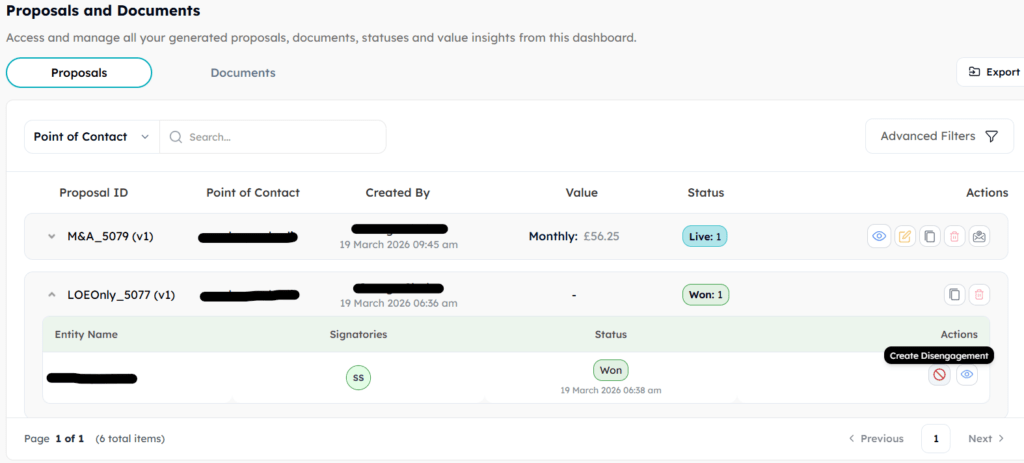

FigsFlow has disengagement letter generation built directly into the platform. When a client relationship ends, you do not open a new document or search for a template. You go to the client’s proposal, hit the disengagement button, and the letter is generated in seconds.

FigsFlow pulls context directly from the original engagement, the services agreed, the proposal number, the dates and the terms, and builds a letter tailored to that specific client and that specific engagement. With over 100 accounting services covered, the letter auto-adjusts to whatever is in scope.

From there, you review, make any final adjustments, and send it to the client in a single click. The whole process takes under two minutes. The letter is compliant, contextual, and ready to go.

Disengagement Letter Resources Worth Bookmarking

- ACCA’s official guidance on ending client relationships, covering your obligations around records transfer, professional clearance, and what to do when a SAR is involved – Disengagement process for corporate clients | ACCA Global

- ICAEW’s official helpsheet on disengagement letters, including guidance on structure, content, and sample wording to help members issue compliant, comprehensive letters – Disengagement letters | Practice helpsheets | ICAEW

Conclusion

A disengagement letter is not paperwork. It is the legal and professional boundary between your responsibility and your former client’s. Get it right, and you walk away clean. Get it wrong, or skip it entirely, and you carry a liability you thought you had left behind.

How you end a client relationship says as much about your practice as how you begin one. The firms that handle both without chaos are the ones that scale. The ones that don’t are still untangling exits from three years ago.

Book a demo and see for yourself how FigsFlow handles your entire client onboarding process, disengagement included.

Frequently Asked Questions(FAQs)

A disengagement letter formally ends the professional relationship between an accountant and their client. It confirms what work has been completed, what remains outstanding, and where your liability stops. Without it, you have no documented proof that the relationship ended, leaving you exposed to complaints, claims, and professional body scrutiny.

Every disengagement letter should cover the effective date, scope of services ending, summary of completed work, outstanding matters, final billing, document transfer arrangements, and a liability disclaimer. Depending on the circumstances, you may also include a reason for disengagement and any critical upcoming deadlines the client needs to be aware of.

State clearly that the engagement is ending and include a specific termination date. Summarise completed work, outstanding obligations, and final fees. Address how records will be transferred. Keep the tone professional and factual regardless of the circumstances. Or use FigsFlow to generate a compliant letter in seconds without starting from scratch.

Have the conversation first, then follow it with the letter. Keep the letter factual and professional. You are not required to apologise or over-explain. State what is ending, when, and what happens next. Firm-initiated exits do not need to be warm, but they should never be hostile.

Your liability does not end until you can prove the relationship was formally closed. Without a letter, you have no documented basis to defend against complaints about missed deadlines or incorrect advice. Your professional indemnity insurer will ask for it if a claim arises. Both ICAEW and ACCA cite failure to disengage properly as a common source of complaints.

No. A signature is best practice and confirms receipt, but it is not required for the letter to be valid. ICAEW guidance confirms that even if a client refuses to sign, the fact that the letter was sent is sufficient to uphold your firm’s position in a dispute. Always keep proof of sending.

No. ACCA’s guidance is explicit: non-payment of fees is not a legitimate reason to withhold records that belong to the client. Financial accounts, tax records, and documents the client commissioned must be returned. Outstanding fees are a separate matter pursued through separate channels, not by holding documents to ransom.

Under Anti-Money Laundering regulations, you are required to retain evidence of client identity for five years from the date the relationship ends. Your wider client file should be kept for at least seven years to cover potential complaints, claims, or subject access requests under data protection legislation.