Got a new job? Congratulations.

You are waiting on that first paycheck, and your employer hands you a stack of paperwork, including a small form, throwing big words at you: pay period, head of household, qualifying surviving spouse, dependents. Overwhelming does not cover it.

Or maybe you are an accountant who needs to complete one for yourself or walk a client through it, and honestly, it is not something you deal with every day. No shame in that. No judgment. We have been there too.

So, no more confusion. In this guide, we walk you through every single step to fill out the 2026 W-4 form correctly, including practitioner flags for dual-income traps and everything that could affect your clients or your own withholding.

What Is the IRS W-4 Form?

The IRS W-4 form is the instruction sheet an employee hands to their employer. It tells them how much federal income tax (the tax the U.S. federal government charges on your earnings, separate from state and local taxes your state or city may also collect) to take out of each paycheck.

Your employer uses the information you provide on IRS W-4 form to calculate your withholding every single pay period. Get it right, and you roughly break even at tax time. Get it wrong and you either owe the IRS (Internal Revenue Service, the U.S. government agency that collects federal taxes) in April or you over-pay all year and wait on a refund that was your money to begin with.

The form was last redesigned in 2020 and no longer uses the old allowances system. If you have a W-4 from before 2020 on file with your employer, it still counts, but the format looks completely different from the current version.

W-4 vs W-4P: Which One Do You Need?

If you receive pension or annuity income (regular payments you receive in retirement from a pension plan, insurance contract, or similar arrangement) rather than wages from an employer, the form you need is the W-4P, not the W-4.

Who Needs to Fill Out an IRS W-4 Form in 2026?

If you just started a new job, recently got married, had a child, picked up a second job, or experienced any major financial change this year, you need to fill out or update your IRS W-4 Form.

Let’s look at each situation in detail.

New Hires

Every new employee must submit a IRS W-4 form before their first paycheck. You do not get a grace period.

There is no penalty for not filling out the form. But if your employer does not have one on file, IRS rules require them to withhold as if you are a single filer with no adjustments, which is the highest withholding rate for your income level. You will likely get that money back as a refund when you file your return, but that is a full year of waiting on your own money, earning little to nothing in return.

Existing Employees with Life Changes

A standard IRS W-4 form stays in effect with your current employer until you submit a new one. There is no automatic expiry, which means a form you filled out years ago at the same job is still controlling your withholding today. Your employer has no way of knowing that it no longer reflects your actual situation.

Life changes can mean you qualify for more or fewer deductions, credits, and adjustments than when you last filled out the form. That directly affects how much tax should come out of each paycheck. If the form does not reflect your current life, your withholding is almost certainly off.

The following events should prompt a IRS W-4 form review:

- Marriage or divorce

- Spouse starts or stops working

- Birth, adoption, or a dependent aging out (a child turns 17 during the year)

- Adding or dropping a second job

- Starting a side business or gig income with no withholding

- Significant change in investment or retirement income

- Home purchase that shifts the itemized deduction calculation

- Major income increase or decrease at either spouse’s job

Keeping your W-4 current ensures your withholding stays close to what you actually owe, so you are not hit with a penalty in April, and your money is not sitting with the IRS all year, earning nothing.

A Note on Tax-Exempt Status

You can claim exemption from withholding if you had zero federal income tax liability in 2025 and expect the same in 2026. The exemption does not carry forward automatically.

You need to resubmit by February 16, 2027, or your employer reverts to the single filer rate with no adjustments.

What Information Do You Need to Fill Out the W-4?

Now that you know whether you need to fill out or update your IRS W-4 form, let’s make sure you have everything on hand before we walk through the form. Nothing worse than getting halfway through and realizing you are missing a number.

Have the following ready:

- Full legal name exactly as it appears on your Social Security card

- Social Security Number (SSN)

- Current mailing address

- Your expected filing status

- Your spouse’s estimated annual wages if you are filing jointly and both of you work

- Number of qualifying children under age 17 and any other dependents

- Estimates of income not subject to withholding: interest, dividends, retirement distributions, 1099 income

- Estimate of your itemized deductions (expenses you plan to claim individually on your tax return, such as mortgage interest, state taxes paid, and charitable donations) if you are not taking the standard deduction

- Your most recent pay stub (the document your employer gives you each pay period, showing how much you earned and how much was withheld), if you are updating the form mid-year

Keep those handy, and let’s get into the form.

A Look at the Full IRS W-4 Form

Below is what the 2026 IRS W-4 form looks like. If you are holding something that looks different, it is likely an older version. Ask your employer for the current one or download it directly from the IRS.

The form is one page with five numbered steps:

- Step 1: Personal Information and Filing Status

- Step 2: Multiple Jobs or Spouse Works

- Step 3: Claim Dependent and Other Credits

- Step 4: Other Adjustments

- Step 5: Sign and Submit

Of the five steps, Steps 2 through 4 are conditional. If you are a single-job employee with no dependents, no side income, and no itemized deductions, you only need to complete Steps 1 and 5. Everyone else works through the relevant steps in between, which is exactly what we cover below.

How to Fill Out the 2026 IRS W-4 Form: Section-by-Section Guide

You have waited long enough. Let’s fill this out, one step at a time, starting with Step 1.

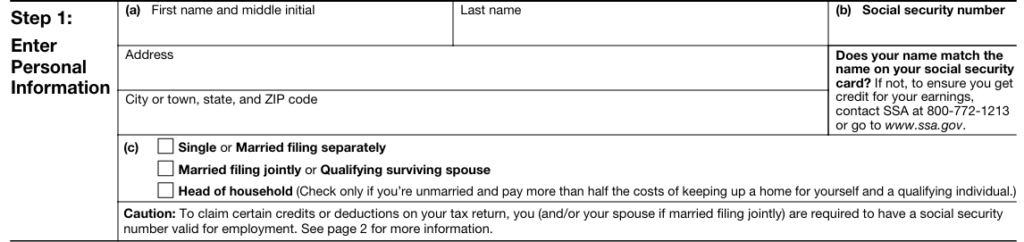

Step 1: Personal Information & Filing Status

Most of this step is basic personal information. Here is what each field is asking for.

Field (a): Name & Address – Enter your full legal name exactly as it appears on your Social Security card, your current mailing address, and your city, state, and ZIP code. This is the address where your employer will send your W-2 in January.

Field (b): Social Security Number – Your SSN must match the name on your Social Security card exactly. If it does not, the Social Security Administration (SSA) cannot credit your earnings to your record, which affects your future Social Security benefits. A transposed digit is enough to cause problems.

Field (c): Filing Status – There are three options in this section:

- Single or Married Filing Separately,

- Married Filing Jointly or Qualifying Surviving Spouse, and

- Head of Household.

Select whichever applies to your situation.

Whatever you choose, make sure it accurately reflects your actual filing status. Providing incorrect information on this form is considered a federal offense under penalties of perjury, as stated on the form itself.

Caution: SSN Valid for Employment

To claim certain credits and deductions on this form, at least one spouse must have a Social Security Number valid for employment. An Individual Taxpayer Identification Number (ITIN) does not count for the purpose of claiming certain credits or deductions. For the Child Tax Credit in Step 3, the qualifying child must also have a valid SSN. For deductions such as qualified tips, overtime, and the senior deduction in Step 4(b), the requirement is that you and/or your spouse have a valid SSN, not necessarily both.

Breaking Down the Terms in Step 1

Single or Married Filing Separately – Single is straightforward. Married Filing Separately means you and your spouse each file your own tax return independently. It can make sense in certain situations, but it usually results in a higher combined tax bill than filing jointly.

Married Filing Jointly – You and your spouse file one combined tax return. This is the most common choice for married couples and gives you access to the widest tax brackets, meaning more of your income is taxed at lower rates.

Qualifying Surviving Spouse – Your spouse passed away recently, and you meet all of the following conditions:

- Your spouse died in 2024 or 2025

- You have not remarried

- You have a dependent child living with you

- You paid more than half the cost of maintaining your home

If all four apply, you can use the same tax brackets as Married Filing Jointly for up to two years after your spouse’s death.

Head of Household – You are unmarried and paid more than half the cost of maintaining a home for a qualifying person, typically a dependent child, for more than half the year. A dependent parent also counts, even if they do not live with you. Being unmarried with children alone does not automatically qualify you. The cost, residency, and dependency conditions all need to be met.

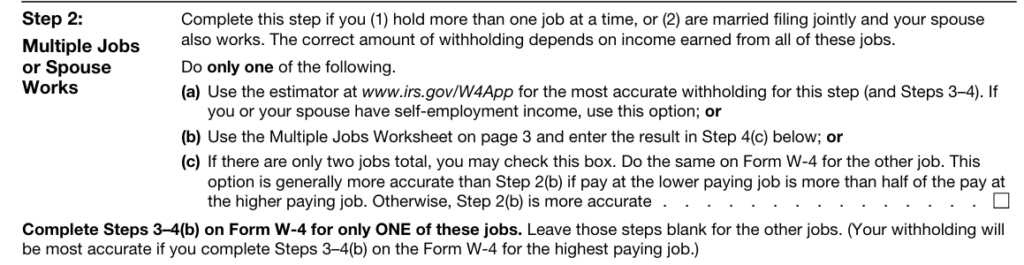

Step 2: Multiple Jobs or Spouse Works

Complete this step if you satisfy either of the following:

- You hold more than one job at the same time

- You are married filing jointly, and your spouse also works

Otherwise, skip this step completely and move to Step 3.

Here is why this step matters. Each employer calculates your withholding as if their paycheck is your only income for the year. When two incomes combine on a joint return, your actual tax bill is higher than either employer assumed. This step tells your payroll system to withhold a little extra to cover that gap.

The form gives you three options. Pick one only.

Option (a): Use the IRS Tax Withholding Estimator – Visit irs.gov/W4App, enter your income details, your spouse’s income if applicable, and any other relevant information. The estimator runs through your full picture and gives you exact figures to enter across Steps 2, 3, and 4, including dependent credits, other income, deductions, and any extra withholding needed. Hold onto those figures. We will need them further down the form.

This is the most accurate Option, especially if you or your spouse has self-employment income alongside regular wages.

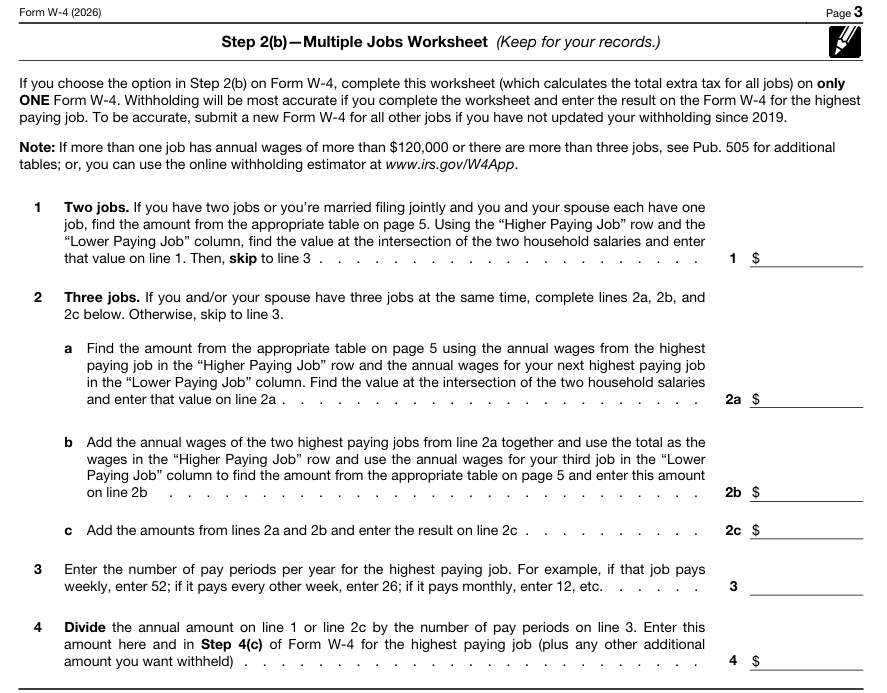

Option (b): Use the Multiple Jobs Worksheet – Scroll down to page 3 of the IRS W-4 form. You will find the Multiple Jobs Worksheet, pictured below.

If you have two jobs, or you and your spouse each have one job, go to the table on page 5 of the form. Find the row that matches the higher-paying job’s annual wages and move across to the column that matches the lower-paying job’s annual wages. The number where those two meet is what you enter on line 1 of the worksheet.

Note: The table on page 5 is only designed for use when the higher-paying job’s annual wages are $120,000 or less. If your higher-paying job earns more than $120,000, use Option (a) instead or refer to IRS Publication 505.

Then on line 3, enter the number of pay periods per year for the higher-paying job. If that job pays biweekly, enter 26. Divide $8,760 by 26, and you get $336.92. That figure goes on line 4 and later into Step 4(c) on the W-4 for the higher-paying job. Keep that number handy.

If you have three jobs, complete lines 2a, 2b, and 2c instead, then skip to line 3.

Option (c): Check the Box – If your household has exactly two jobs total, you can simply check this box. Do the same on the other W-4 as well. Both of you need to check it.

This Option works well when both jobs pay similar amounts. If one job pays significantly more than the other, Option (b) gives you a more accurate result. The bigger the income gap, the more Option (c) tends to over-withhold.

Breaking Down the Terms in Step 2

Self-Employment Income – Money you earn working for yourself, including freelance work, contract jobs, gig work, or running your own business. Unlike regular wages, no tax is withheld automatically, which is why Option (a) is recommended if this applies to you.

Pay Period – How frequently your employer pays you. The number of pay periods per year affects the worksheet calculation in Option (b).

- Weekly: 52 pay periods per year

- Biweekly (every two weeks): 26 pay periods per year

- Semimonthly (twice a month): 24 pay periods per year

- Monthly: 12 pay periods per year

Step 4(c) Extra Withholding – This is where the figure from Option (b) lands on the main form. If you completed the Multiple Jobs Worksheet, take the number from line 4 and enter it here. If you used Option (a), the estimator provides individual figures for Steps 3, 4(a), 4(b), and 4(c) separately. Enter each figure into its corresponding step on the form, not all into Step 4(c). More on that when we get there.

Step 3: Claim Dependent & Other Credits

Complete this step if you satisfy both of the following:

You have qualifying children under age 17 or other dependents

- Your total household income is $200,000 or less (or $400,000 or less if married filing jointly)

- If your income is above those thresholds, skip this step entirely and move to Step 4.

This step is straightforward. Here is what goes where.

Line 3(a) – Multiply the number of qualifying children under age 17 by $2,200. Enter the total.

Line 3(b) – Multiply the number of other dependents (anyone who does not qualify as a child under 17, such as a dependent aged 17 or older, an elderly parent you support, or another qualifying relative living in your household) by $500. Enter the total.

Line 3 – Add the amounts from 3(a) and 3(b) together and enter the combined total here.

Dual-Income Households: Only One Spouse Completes Step 3

If both you and your spouse work, only one of you should complete Step 3 on the W-4 for the highest-paying job. If both of you enter your children on your respective forms, both employers reduce withholding by the full credit amount. But the credit only appears once on your joint return. The result is a gap between what was withheld and what you actually owe, and that gap can easily reach several thousand dollars, plus potential underpayment penalties come April.

Breaking Down the Terms in Step 3

Qualifying Child – To count a child in line 3(a), all of the following must be true:

- The child is under age 17 as of December 31, 2026

- The child lives with you for more than half the year

- You claim the child as a dependent on your tax return

- The child has a Social Security Number valid for employment (an ITIN does not count here)

Example – You have two children aged 9 and 13, and one dependent parent aged 71.

- Line 3(a): 2 children x $2,200 = $4,400

- Line 3(b): 1 other dependent x $500 = $500

- Line 3 total: $4,900

The qualifying child multiplier increased from $2,000 to $2,200 for 2026.

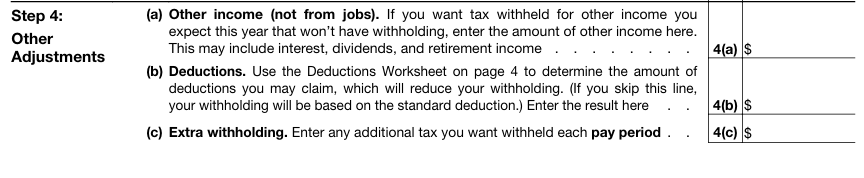

Step 4: Other Adjustments

All three sub-steps here are optional. Complete whichever ones apply to your situation.

Line 4(a): Other Income Not from Jobs – If you expect income in 2026 that will not have any tax withheld automatically, enter the annual estimated amount here. This includes interest, dividends, retirement distributions, rental income, and any 1099 income from freelance or contract work. Your employer will factor this into your withholding so that tax on that income gets covered throughout the year instead of landing as a surprise bill in April.

Line 4(b): Deductions Worksheet – If you plan to claim deductions beyond the standard deduction, complete the Deductions Worksheet on page 4 of the form and enter the result here. Skipping this line means your withholding will be based on the standard deduction only.

Line 4(c): Extra Withholding Per Pay Period – If you completed the Multiple Jobs Worksheet in Option (b) back in Step 2, the figure from line 4 of that worksheet goes here. If you used the Tax Withholding Estimator in Option (a), it provides separate figures for Steps 3, 4(a), 4(b), and 4(c) individually. Enter each figure into its corresponding step, not all into this line.

You can also use this line even if Step 2 did not apply to you. If you simply want a little extra withheld each paycheck as a cushion, enter whatever amount works for you. It reduces your paycheck slightly but means a smaller bill, or a larger refund, when you file.

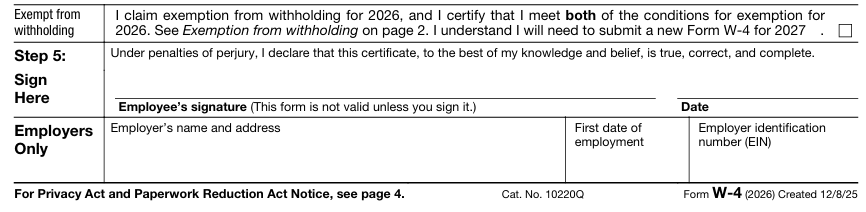

Exempt from Withholding

You qualify for exempt status if both of the following are true:

- you had no federal income tax liability in 2025, and

- you expect none in 2026.

If both apply, check the box in the Exempt from Withholding section, complete only Steps 1(a), 1(b), and 5, and leave everything else blank.

The exemption does not carry forward. You need to resubmit by February 16, 2027, or your employer reverts to the single filer rate with no adjustments.

2026 Deductions Worksheet: What’s New

The 2026 worksheet includes three deductions that were not on the 2025 form:

- Qualified tips: up to $25,000, if your total income is below $150,000 ($300,000 MFJ)

- Qualified overtime compensation: the extra “and-a-half” portion of time-and-a-half pay, up to $12,500 ($25,000 MFJ), same income threshold

Qualified passenger vehicle loan interest: interest on a loan for a new, U.S.-assembled vehicle, up to $10,000, if your income is below $100,000 ($200,000 MFJ)

It also includes a senior deduction of $6,000 if you will be 65 or older by December 31, 2026, and another $6,000 for your spouse under the same condition, available when total household income is below $75,000 ($150,000 MFJ).

2026 Standard Deductions for Reference – The following figures are taken directly from line 11 of the 2026 IRS W-4 form Deductions Worksheet:

- Married Filing Jointly or Qualifying Surviving Spouse: $32,200

- Head of Household: $24,150

- Single or Married Filing Separately: $16,100

Step 5: Sign and Submit

Almost done. This step has two parts, depending on who is filling it out.

If You Are the Employee – Sign and date the form. That is it. Without a signature, the form is not valid, and your employer will treat you as a single filer with no adjustments. Hand the completed form to your HR or payroll department. It does not go to the IRS, and you do not attach it to your tax return.

If You Are the Employer – The “Employers Only” section at the bottom is yours to complete. Fill in your business name and address, along with two fields:

- First date of employment – the date this employee officially started working for you

- Employer Identification Number (EIN) – the tax identification number assigned to your business by the IRS

As an employer, you are required to apply the updated IRS W-4 form within one to two payroll cycles of receiving it.

Common W-4 Mistakes to Avoid

Across the employees and clients we have worked with, we see the same patterns come up again and again. A step skipped, a field left blank, a form never updated after a life change. Small things that quietly produce the wrong withholding for months, sometimes years.

Here are the five mistakes that show up most often.

Skipping Step 2 in a Dual-Income Household

If you check “married filing jointly” in Step 1 but leave Step 2 blank, each employer assumes they are your only income source. Neither withholds enough. When your combined income hits a joint return, the shortfall shows up as a tax bill, often with an underpayment penalty attached.

Both Spouses Completing Step 3

Only one spouse should complete Step 3. If both of you enter your children on your respective W-4s, both employers will reduce withholding for the full child tax credit. The credit appears once on your joint return. The math does not close, and April gets expensive.

Not Updating After a Life Change

Your IRS W-4 form does not expire, and no one reminds you to update it. A form you filled out at your last job, before your marriage or before your second child, is still controlling your withholding today. Review it any time your financial situation changes.

Ignoring the 2026 Deductions Worksheet

If you earn tips or overtime and your income falls below the applicable threshold, you now qualify for deductions that were not on the 2025 form. Skipping Step 4(b) means your withholding does not account for them, and you leave money on the table until you file.

Not Signing the Form

A IRS W-4 form without a signature is treated as if it were never submitted. Your employer defaults to single filer with no adjustments. It sounds obvious, but it is one of the most common issues on a new hire’s first day.

Conclusion

For fairly straightforward scenarios, this guide should be more than enough. The IRS W-4 form is a simple form at its core, and most people will find their situation covered somewhere above.

That said, the Deductions Worksheet on page 4, the Multiple Jobs Worksheet on page 3, and a handful of other situations can make things genuinely complicated. We have covered them here, but words on a screen only go so far.

If you are still unsure after going through this, that is completely okay. Talk to your HR or payroll officer. That is exactly what they are there for, and they can walk you through it in a way that a guide simply cannot.

Frequently Asked Questions (FAQs)

Most employees do not have to resubmit annually unless their financial situation changes. The one exception is tax-exempt employees, who must submit a new IRS W-4 form by February 16 each year or lose their exempt status for that tax year. Everyone else should revisit the form any time income, filing status, or dependents change.

Your employer is required to withhold as if you are a single filer with no other adjustments. For a married employee with children and a working spouse, this almost always results in over-withholding, meaning your paychecks are smaller than they need to be. For a single-job employee, the default may actually approximate the correct amount, but it is never guaranteed.

Yes. Employees may submit an updated IRS W-4 form at any time during the year, as many times as needed. The employer must apply the change within a reasonable period, typically one to two payroll cycles. The change applies only to pay periods after the updated form is received. It does not retroactively adjust what was already withheld earlier in the year.

A qualifying surviving spouse is a widowed taxpayer whose spouse died in 2024 or 2025, who has not remarried as of December 31, 2026, and who maintains a home for a dependent child who lived there for the full year. This status allows the surviving spouse to use the Married Filing Jointly tax brackets for up to two years after the year of the spouse’s death, which is a meaningful tax benefit.

The 2026 W-4 has five steps. Enter your personal information and filing status in Step 1, account for multiple jobs or a working spouse in Step 2, claim dependents in Step 3, make any additional adjustments in Step 4, and sign in Step 5. Steps 2 through 4 are only completed if they apply to you.

Enter an additional dollar amount in line 4(c) under Extra Withholding. This increases the federal tax taken out of each paycheck, which means a larger refund when you file. Just remember that the refund is your own money coming back to you, not a bonus.

Any employee starting a new job needs to complete a IRS W-4 form before their first paycheck. Beyond that, anyone whose financial situation has changed since they last filled one out, whether through marriage, a new child, a second job, or a significant income change, should update theirs.

If you are married and plan to file jointly, selecting that status results in less tax being withheld from each paycheck. However, if your spouse also works and you skip Step 2, you will likely be under-withheld. Your filing status should always reflect your actual situation, not what produces the smallest withholding.