700,000 sole traders and landlords entered MTD from April 2026. Another million follows in April 2027. Each one needs to be segmented, priced, engaged, AML-checked, authorised, and signed up before their first quarterly deadline.

A practice with 100 mixed-income clients is looking at 800 quarterly updates. That is the ongoing work. The harder part is getting there: onboarding MTD clients in the next twelve months, more than most firms have taken on in the last five years combined, using a manual process that was already slow at annual volume.

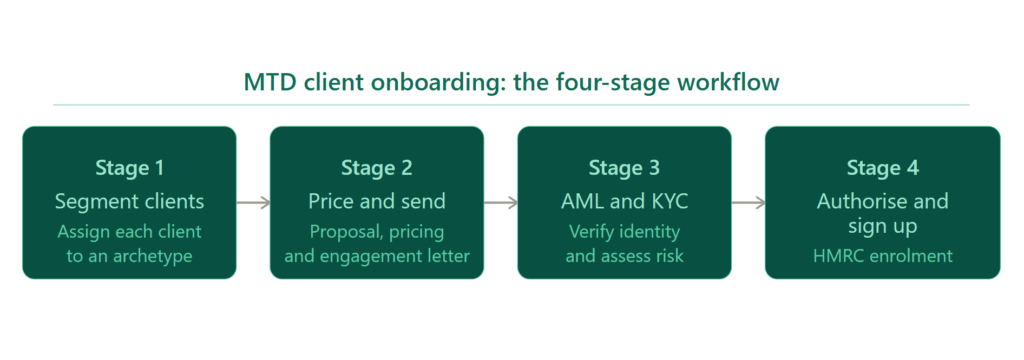

This guide covers the full MTD client onboarding workflow in the order you run it. Segment first, then price and send, then AML and KYC, then authorise and sign up. Stay to the end, there is up to 50% off the tools that run it.

Before you dive in: This guide assumes you know what MTD for Income Tax is and who it affects. If you are starting from scratch, read this first: MTD ITSA Guide for Accountants and Tax Agents 2026

Segment Your Client Book First

Export every Self Assessment client with qualifying income from the 2024/25 return. Flag who is in scope by threshold and year:

- above £50,000 for April 2026,

- above £30,000 for April 2027,

- above £20,000 for April 2028.

Then assign each in-scope client to an archetype using the three segmentation axes below.

MTD client segmentation comes first because pricing, engagement letters, and capacity planning all depend on it. A practice that skips it ends up pricing a freelance consultant and a portfolio landlord on the same basis, and the complex one gets underpriced.

The Three Segmentation Axes

Three variables determine what an MTD client actually costs to serve.

Complexity covers income sources, ownership structure, and cross-source combinations. For sole traders: single trade versus multiple streams, employees, VAT, CIS. For landlords: number of properties, sole versus joint ownership, UK versus mixed UK and foreign, Section 24 applicability. The highest-complexity clients are those with both: a sole trader who also lets property, or a landlord who also trades.

Digital capability determines who does the bookkeeping. A consultant who invoices through an app and categorises their own bank feeds is a fundamentally different service model from a tradesperson with a carrier bag of receipts. Client self-entry costs the firm far less than firm-managed bookkeeping.

Transaction volume drives time, which drives the fee. A sole trader with one client may have 20 transactions a year. A multi-property landlord can have hundreds.

The 6 MTD Client Archetypes

| Archetype | Typical Profile | Service Model |

|---|---|---|

| Simple Sole Trader | Single trade, low volume, digitally confident | Client self-entry; firm reviews and files quarterly |

| Simple Landlord | 1 to 2 BTLs, sole ownership, basic-rate taxpayer | Bank feeds capture most transactions; firm reviews and files |

| Complex Sole Trader | Higher volume, subcontractors, CIS, stock or WIP | Firm manages or heavily reviews bookkeeping |

| Portfolio Landlord | 5 to 15 properties, joint ownership, Section 24 material | Firm manages bookkeeping, letting agent imports, advisory calls |

| Multi-Source | Self-employment plus property, two or more quarterly obligation sets | Parallel records per business; two sets of quarterly updates |

| HNW / Complex | Mixed sources, foreign property, Form 17 elections, advisory embedded | Dedicated client manager, bespoke quarterly reporting |

Once every in-scope client has an archetype, you have an estimated time budget for each client and a clear picture of where capacity is tested. That is the foundation for pricing.

Segmentation also means deciding who you will not serve. A generalist firm that cannot handle complex property quarterly mechanics can refer that work to a specialist as Supporting agent while retaining the client relationship as Main agent. Design your exclusions deliberately rather than discovering them mid-engagement.

Price, Scope & Send in One Step

Under Self Assessment, a flat fee per return type was defensible. One return, once a year, broadly predictable scope. Under MTD, that breaks because the Final Declaration is where client-specific complexity multiplies, and two clients with identical quarterly updates can have Final Declarations that are worlds apart.

Take two buy-to-let landlords. One has property income only, basic-rate taxpayer, straightforward year-end. The other has employment income, dividends, capital gains, and carried-forward losses. Their quarterly update workload is identical. Their Final Declaration is not even close. Pricing them the same means one client subsidises the other, and it is always the complex one you undercharge.

The Variables That Set the Price

Every MTD fee has two components: the cost of delivering quarterly updates, and the cost of delivering the Final Declaration. The variables below drive each.

Quarterly Update Variables

| Factor | Effect on Price |

|---|---|

| Number of qualifying businesses | Additional fee per business |

| Number of properties | Additional fee per property |

| Joint ownership | Significant uplift |

| Foreign property | Significant uplift |

| Letting agent managed vs self-managed | Agent-managed reduces the bookkeeping overhead |

| Client digital capability | Firm-led bookkeeping increases cost |

Final Declaration Variables

| Factor | Effect on Price |

|---|---|

| PAYE employment income | Moderate uplift |

| Dividend and savings income | Moderate uplift |

| Capital gains | Significant uplift |

| Double tax relief for foreign property | Significant uplift per country |

| Loss relief claims | Moderate to significant uplift |

| Gift Aid, EIS, SEIS, Marriage Allowance | Per relief type |

Select the relevant variables for a specific client, and the price is determined by the combination.

For the full pricing framework with fee structures, archetypes, and worked examples, read our complete guide on how to price MTD ITSA services.

Combining the Proposal & Engagement Letter

Treat the MTD engagement letter and proposal as one document. Or, at the very least, send them together.

The client reads the proposal, accepts the scope and fee, and signs the engagement in the same step. Two separate documents mean two rounds of chasing signatures.

An MTD-ready proposal covers six elements:

- A plain-language scoping summary: what the client has and what the firm will do

- A services inclusion table with explicit in-scope and out-of-scope items

- A fee summary with both monthly and annual figures visible

- A timeline from proposal acceptance to first quarterly deadline

- Out-of-scope triggers that cause a re-price

- Engagement letter terms with e-signature

The MTD engagement letter needs to cover what existing Self Assessment letters do not: four quarterly updates per qualifying business, listed separately from the Final Declaration; the client’s data cut-off obligations each quarter; how quarterly approval before filing works; the billing model; re-quote triggers; and automated payment collection. An annual direct debit or monthly subscription eliminates the need to chase quarterly invoices on top of quarterly data chasing.

Re-papering existing clients before their first quarterly deadline is not negotiable. A self-assessment engagement letter does not describe the MTD deliverables, does not specify the agent role, and leaves the fee basis open for a service that now involves five filings a year instead of one.

Read our complete guide on the MTD engagement letter for what to update in your SA engagement letter for MTD ITSA.

Run AML & KYC at Scale

Every new MTD client, and every existing client being re-papered into MTD, is subject to your firm’s AML obligations. The Money Laundering Regulations 2017 require, at a minimum:

- Identification of the client verified against a reliable independent source

- Risk assessment of the client and the engagement, retained with the firm

- Ongoing monitoring of the relationship

- Records kept for at least five years from the end of the engagement

For a UK-resident individual landlord or sole trader, the standard KYC checks are:

- Photo ID: passport or photocard driving licence, electronically verified

- Proof of address dated within three months

- For landlord clients, confirmation of property ownership

The checks themselves have not changed. The volume has. At 80 new MTD clients per year, at a conservative two hours of AML, KYC, risk assessment, and EDD time per client, the firm absorbs 160 fee-earner hours on onboarding MTD clients before a single engagement generates margin. Building that into your MTD workflow for accountants is not optional.

Joint Ownership: Verify All Beneficial Owners

With joint ownership, the obligation is to verify all beneficial owners, not just the lead contact. A couple jointly owning three properties requires two sets of ID verification, two proof-of-address checks, and potentially two separate engagement letters if their qualifying income figures put them in different mandation years. The lead contact signing the proposal does not satisfy the AML requirement for the co-owner.

When EDD applies

Enhanced Due Diligence applies when the risk assessment indicates a high risk. The triggers to build into your workflow:

- Politically Exposed Persons and their close associates

- Clients with material assets in higher-risk jurisdictions

- Complex ownership structures including trusts and offshore companies

- Clients whose source of funds for property purchases is not obvious from their declared income

Document the judgment. A structured EDD template, completed and retained, is what shows your AML supervisor that you assessed the risk properly before taking the client on.

Authorise & Sign Up Each Client

Authorisation and sign-up are two separate steps, and conflating them is one of the most common errors in MTD ITSA agent authorisation. Authorisation means HMRC recognises your firm as the client’s agent. Sign-up means the client has been enrolled into the MTD regime and has quarterly obligations. Both must be in place before the first quarterly update can be filed.

Existing Self Assessment authorisations, whether 64-8 or Government Gateway, do not transfer automatically. You must actively add them to your Agent Services Account. The authorisation itself transfers without a fresh client consent process, but skipping the ASA step locks you out of filing for clients you may have acted for since 2002.

What You Need Before Each Sign-Up

Gather the following for each client before initiating the sign-up:

- National Insurance number

- UTR (10 digits)

- Date of birth and full address as held by HMRC

- Agent Services Account credentials

- Details of each qualifying source: trade name or property type, start date, accounting basis, and accounting period end

- An accounting-basis decision per business (cash basis is the default; no turnover threshold applies)

- A quarter-election decision: tax-year quarters or calendar-quarter election

- Compatible MTD software chosen and approved by the client before sign-up

There is no bulk sign-up API. HMRC designed sign-up as a one-at-a-time process. A practice onboarding 200 new MTD clients runs 200 individual sign-ups. Build that into your capacity plan now.

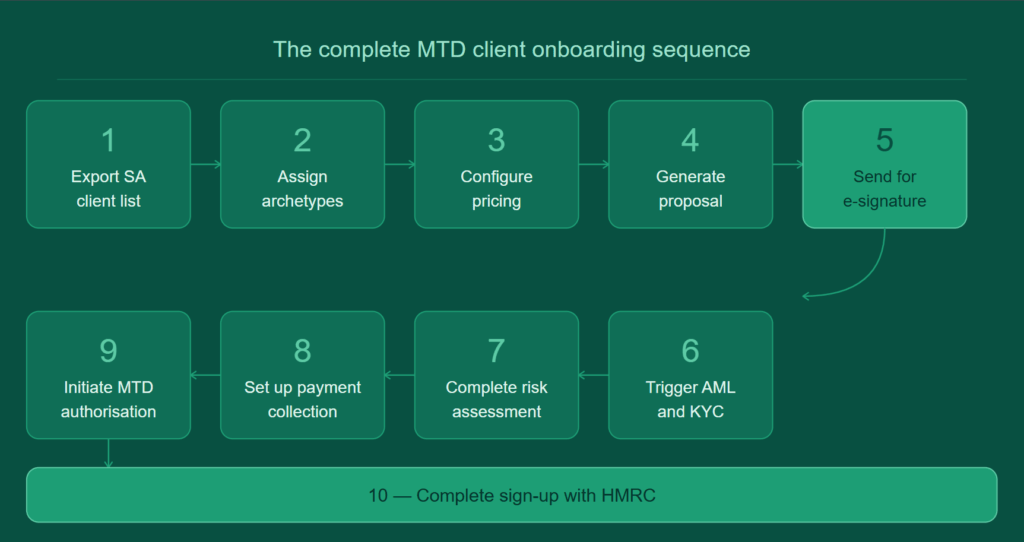

What the Full MTD Client Onboarding Sequence Looks Like

Done properly, this takes 10 to 15 minutes of actual firm time per client. At that pace, a firm onboards 28 clients in a working day. The pre-MTD manual process ran at two clients a day at best.

Tools That Make Onboarding MTD Clients Scalable

All of the above is useful knowledge. But knowing the workflow and running it efficiently are two different things. Done manually, across any meaningful volume of MTD clients, the process grinds.

That is where FigsFlow and RentalBux come in. Together, they cover the complete journey from first contact through to quarterly submissions and the Final Declaration. Nothing falls between systems.

FigsFlow handles the front office. Proposals, pricing, MTD engagement letters, AML and KYC, payment collection. All in one place. Accountants who use it rate it 5.0 on G2 and 4.9 on Trustindex. It won Proposal Software of the Year and AML/KYC Solution of the Year at the 2026 SME 500 UK Awards.

RentalBux is a different beast. Where FigsFlow deals with the onboarding side, RentalBux is the compliance engine: digital records, quarterly MTD submissions, the Final Declaration, and a practice dashboard that gives you visibility across every client. HMRC-recognised. FCA registered. Built specifically for property and mixed-income clients, which is most of your MTD book.

Through the FigsFlow and RentalBux partner programme, accountants can access discounts of up to 50% on client plans, among other benefits.

Want to know what that looks like for your firm? Book a demo and speak to the team directly.

Conclusion

The sequence is fixed. Segment, price and send, AML and KYC, authorise and sign up. Get it right on the April 2026 cohort and it holds when the April 2027 wave arrives. Leave it until the volume forces the issue and you are rebuilding under pressure.

Try FigsFlow free for 30 days and onboard your first batch of MTD clients.

Frequently Asked Questions (FAQs)

With a manual process, separate proposals, separate engagement letters, a separate AML tool, and payment setup done independently, onboarding a single MTD client takes a minimum of two hours. Most practices report closer to two and a half. With dedicated onboarding software like FigsFlow, the same steps take 10 to 15 minutes of actual firm time.

Authorisation means HMRC recognises your firm as the client’s agent for MTD ITSA services. Sign-up means the client has been enrolled into the MTD regime and has quarterly obligations. Both must be in place before the first quarterly update can be filed. They are separate steps and completing one does not complete the other.

Yes. New clients require full verification: photo ID, proof of address, and a completed risk assessment before the engagement is signed. Existing clients being re-papered into MTD need, at a minimum, a refreshed risk assessment. If their records are out of date, circumstances have changed, or a periodic review is overdue, full re-verification applies. The Money Laundering Regulations 2017 make no exception for MTD, nor is there an exemption for long-standing clients.

No. HMRC designed the sign-up as a deliberate one-at-a-time process. There is no bulk sign-up API. A practice onboarding 200 MTD clients runs 200 individual sign-ups. Each requires the client’s NI number, UTR, date of birth, address as held by HMRC, and details of each qualifying income source.

An MTD engagement letter should cover: the scope of services listing each qualifying business and its quarterly updates separately from the Final Declaration, the client’s data obligations each quarter, how quarterly approval before filing works, the agent role (Main or Supporting), the fee arrangement with explicit re-quote triggers, and data ownership provisions for the digital records held in software.

Start by assigning each client to an archetype based on their income sources, ownership structure, and digital capability. Then apply a variable framework: set a base fee for the quarterly updates driven by transaction volume and number of qualifying businesses, and price the Final Declaration separately based on the client’s specific income sources and relief claims. The two components combined produce a client-specific fee rather than a flat rate applied across the board.