With Form 4868, you can file a tax extension for up to six months. To do this, you estimate your 2026 tax liability, enter what you have already paid, remit any remaining balance you can, and file the form by April 15, 2027. The IRS automatically extends your filing deadline to October 15, 2027, no explanation required.

But here is the catch. There is no extension to the payment. Any tax owed is still due April 15, 2027. Miss that, and interest starts accruing from that date. The late payment penalty may follow on top of it.

That is what this guide is about. Whether you are an accountant filing extensions for clients or a taxpayer working through this yourself, this guide covers everything about Form 4868: what it is, what it does, who can use it, and how to complete it correctly so the extension holds.

What Is Form 4868 (& What Does Form 4868 Look Like)?

Form 4868 is the IRS application for an automatic extension of time to file a US individual income tax return.

Here is what the form looks like.

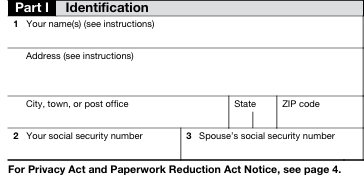

The form is divided into two parts.

- Part I Covers Identification – your name, address, and Social Security Number (SSN).

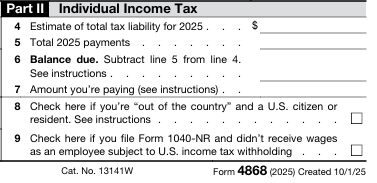

- Part II Covers the Tax Calculation – your estimated total liability, payments already made, the resulting balance, and the amount you are remitting with the extension.

What Form 4868 Does (& Doesn't Do)?

Form 4868 eliminates the late filing penalty. It does not touch the late payment penalty or interest.

Form 4868 extends the time to file your return by up to six months. For the 2026 tax year, the deadline to file is April 15, 2027. If you file Form 4868 before that date, you can file your tax return as late as October 15, 2027. However, you still need to pay your taxes by April 15, 2027.

Failing to pay by April 15 means interest starts accruing on any unpaid balance from that date. The late payment penalty may apply on top of it. The only thing Form 4868 eliminates is the late filing penalty.

Refer to the table below for what happens to your tax filing for the 2026 tax year, with and without a Form 4868 extension.

| Without Extension | With Form 4868 | |

|---|---|---|

| Deadline to file | April 15, 2027 | October 15, 2027 |

| Deadline to pay | April 15, 2027 | April 15, 2027 (unchanged) |

| Interest on unpaid tax | Starts April 15, 2027 | Starts April 15, 2027 |

| Late payment penalty | Applies | Applies if under 90% paid |

| Late filing penalty | Applies | Waived if filed by Oct 15, 2027 |

Who Can File Form 4868?

Form 4868 is available to any taxpayer filing Form 1040, Form 1040-SR, Form 1040-NR, or Form 1040-SS. Filing the extension also automatically extends the deadline to file Form 709 for the same tax year, but it does not extend the time to pay any gift or GST tax owed. Fiscal year taxpayers may also use Form 4868, but must file on paper.

There are two situations where Form 4868 cannot be used:

- The taxpayer is under a court order to file by the original deadline.

- The taxpayer wants the IRS to calculate their tax for them.

Key Terms

- Form 1040 – Standard US individual income tax return filed by most taxpayers

- Form 1040-SR – Filed by senior taxpayers born before January 2, 1962.

- Form 1040-NR – Filed by nonresident aliens with US tax obligations.

- Form 1040-SS – Filed by self-employed residents of US territories.

- Form 709 – Gift and Generation-Skipping Transfer (GST) tax return.

Three Ways to Request the Tax Extension

The three ways to file a tax extension in the US are:

- Pay electronically and skip the form entirely

- E-file Form 4868 through tax software or a professional e-file system

- File Form 4868 on paper and mail it to the IRS

Let us look at each one in detail.

Option 1: Pay Electronically & Skip the Form

If you make an electronic payment toward your 2026 estimated tax liability and select “extension” as the reason, the IRS processes the extension automatically. No Form 4868 is required. Accepted payment methods include IRS Direct Pay, the Electronic Federal Tax Payment System (EFTPS), debit card, credit card, and digital wallets such as PayPal and Venmo.

This Option Requires an Actual Payment. If you owe nothing because withholding and estimated payments already cover the full liability, this option is not available. File Form 4868 instead

Option 2: E-file Form 4868

You can file Form 4868 electronically and receive an electronic acknowledgment on completion. Retain it. That acknowledgment is your proof that the extension was filed on time.

The electronic form is available at irs.gov/FreeFile, or you can file through an IRS-approved tax software or professional e-file system.

Fiscal Year Taxpayers Cannot E-file

A fiscal year taxpayer is someone whose tax year ends on a date other than December 31. If that applies to you, this route is not available. You must file Form 4868 on paper.

Option 3: File Form 4868 on Paper

You can download Form 4868 directly from irs.gov/Form4868. Once you fill in the form, mail it to the IRS address for your state, or your client’s state if you are filing on their behalf. Enclose a check or money order if making a payment.

If mailing via a private delivery service such as UPS, FedEx, or DHL, use the street address listed at irs.gov/PDSStreetAddresses. Private delivery services cannot deliver to PO boxes.

Where to Mail Form 4868

| If you live in | With payment, mail to | Without payment, mail to |

|---|---|---|

| AL, FL, GA, LA, MS, NC, SC, TN, TX | PO Box 1302, Charlotte, NC 28201-1302 | Austin, TX 73301-0045 |

| AZ, AR, NM, OK | PO Box 931300, Louisville, KY 40293-1300 | Austin, TX 73301-0045 |

| CT, DE, DC, IL, IN, IA, KY, ME, MD, MA, MN, MO, NH, NJ, NY, PA, RI, VT, VA, WV, WI | PO Box 931300, Louisville, KY 40293-1300 | Kansas City, MO 64999-0045 |

| AK, CA, CO, HI, ID, KS, MI, MT, NE, NV, ND, OH, OR, SD, UT, WA, WY | PO Box 931300, Louisville, KY 40293-1300 | Ogden, UT 84201-0045 |

| Foreign country, American Samoa, Puerto Rico, APO/FPO address, or Form 2555/4563 filers | PO Box 1303, Charlotte, NC 28201-1303 USA | Austin, TX 73301-0215 USA |

What Information Do You Need to Complete Form 4868?

Before you complete the form, you need to have the following information in place:

- Your full legal name as it appears on prior returns. For a joint extension, both spouses’ names in the order they will appear on the actual return

- Current mailing address. If the address has changed since the last return, note that a new address on Form 4868 does not update IRS records. That requires a separate Form 8822

- Social Security Number (SSN). For a joint extension, both SSNs are required. Non-resident and resident aliens without an SSN use their Individual Taxpayer Identification Number (ITIN)

- An estimate of your total 2026 tax liability. The figure you expect to appear on Form 1040, line 24. This must be reasonable. An unreasonable estimate can void the extension

- Total payments already made in 2026. Federal income tax withheld from wages and any estimated tax payments made during the year

- The amount being paid with the extension, if any. Payment is not required to get the extension

How to Complete Form 4868 (Step by Step)

Form 4868 is divided into two parts. Part I requires your identification details: your name, address, and Social Security Number. Part II requires your tax figures: your estimated total liability, payments already made, the balance due, and the amount you are remitting with the extension. Fill in both parts, send it to the IRS, and you are done.

Let us look at each part and see how to fill it in accurately.

Part I: Identification (Lines 1 to 3)

Line 1: Name & Address

Enter the client’s name and current mailing address. For a joint return, enter both spouses’ names in the same order they will appear on the return. If correspondence should go to an agent rather than the client directly, include both the agent’s and the client’s names, along with the agent’s address.

Line 2: Your Social Security Number

For a single filer, this is the client’s SSN. For a joint return, enter the SSN that will appear first on the return. If filing Form 1040-NR on behalf of an estate or trust, enter the Employer Identification Number (EIN) instead, and write “estate” or “trust” in the left margin next to it.

Line 3: Spouse's Social Security Number

If you are filing a joint return, enter the spouse’s SSN here in the same order it will appear on the actual return.

Two Things to Get Right Before Moving On

- Name Change.

If your client’s name has changed since the last return, the SSA must be notified before Form 4868 is filed. Filing under a name the SSA has not yet updated creates a mismatch that delays processing of the extension request. - Address Change.

A new address entered on Form 4868 does not update the client’s IRS records. If the address changed, file Form 8822 separately. The IRS will continue sending correspondence to the old address on file until Form 8822 is processed.

Part II: Individual Income Tax (Lines 4 to 9)

Line 4: Estimate of Total Tax Liability for 2026

Enter the total tax you expect to report on your return for 2026. If the expected liability is zero, enter 0. You can round all amounts to whole dollars, but apply it consistently across every line.

When the Extension Becomes Void

If the IRS determines the estimate on line 4 was not reasonable given the information available at the time of filing, the extension is invalid. The late filing penalty then applies from April 15, 2027.

Line 5: Total 2026 Payments

Enter the total tax payments already made during 2026. This covers federal income tax withheld from your wages and any estimated tax payments made throughout the year. You can find your withholding figure on your W-2. For estimated tax payments, check your IRS online account at irs.gov or your own payment records.

Line 6: Balance Due

This is the difference between your estimated total tax liability (line 4) and the payments you have already made (line 5). Subtract line 5 from line 4. If the result is positive, you owe that amount. If line 5 is greater than line 4, enter zero.

Line 7: Amount Being Paid

Enter the amount you are paying with this extension. Payment is not required to obtain the extension, but paying as much as possible by April 15, 2027, reduces the accrual of interest on any unpaid balance. Any amount paid here is credited against your final tax liability when you file your return.

The 90% Safe Harbour Rule

The late payment penalty is waived if at least 90% of the tax liability is paid by April 15, following the tax year-end, through withholding, estimated tax payments, or a payment made with Form 4868, and the remaining balance is paid when the return is filed.

Line 8: Out of the Country Checkbox

Check this box if you are a US citizen or resident who, on the due date of the return, lives and works outside the US and Puerto Rico, or is on active military or naval duty outside those areas.

If this applies to you, you already receive an automatic two-month extension to June 15, 2027, without filing anything. Filing Form 4868 and checking this box by June 15, 2027 extends your filing deadline by a further four months, to October 15, 2027. Interest still accrues from April 15, 2027 regardless.

Line 9: Form 1040-NR Checkbox

Check this box if the client files Form 1040-NR, did not receive wages subject to US income tax withholding, and their return is due June 15, 2027.

What Are the Deadlines for Filing Form 4868?

Form 4868 must be filed by the due date of the return it is extending. For most individual filers, that is April 15, 2027. Filing after that date, even by one day, means the extension is not valid and the late filing penalty applies from the original deadline.

The table below outlines the Form 4868 filing deadlines for the 2026 tax year.

| Filer Type | Original Return Due | Form 4868 Must Be Filed By | Extended Filing Deadline |

|---|---|---|---|

| Standard calendar year filers | April 15, 2027 | April 15, 2027 | October 15, 2027 |

| Out of the country (US citizen or resident) | June 15, 2027 | June 15, 2027 | October 15, 2027 |

| Form 1040-NR without US wage withholding | June 15, 2027 | June 15, 2027 | October 15, 2027 |

| Fiscal year taxpayers | Varies | By the fiscal year return due date | 6 months from due date |

Common Mistakes When Filing Form 4868

Form 4868 is a short form, but a few errors come up repeatedly and some of them are costly. Here are the most common ones to watch out for.

- Treating the Extension as a Payment Extension

The extension moves the filing deadline, not the payment deadline. Interest and the late payment penalty both begin on April 15, 2027, on whatever balance was not paid by that date. - Entering Zero on Line 4 Without Justification

If you have income, entering zero signals an unreasonable estimate. The IRS can void the extension on that basis, and the late filing penalty applies from April 15, 2027. - Including the Form 4868 Payment on Line 5

Line 5 is for payments already made during 2026. The amount being paid with this extension goes on line 7. Entering it on line 5 distorts the entire Part II calculation. - Filing the Paper Form After April 15, 2027

A paper form postmarked April 16 does not extend anything. If filing close to the deadline, use a designated private delivery service with tracking. - Not Retaining the E-file Acknowledgment

The acknowledgment is your proof that the extension was filed on time. Without it, demonstrating timely filing becomes difficult if the IRS later questions it.

What Happens After You File Form 4868?

Filing Form 4868 is not the end of the process. You still need to file your actual 2026 return before October 15, 2027. The return can be filed any time before that date.

Any amount paid with Form 4868 is automatically credited against your final tax liability when you file your return, unless the IRS denies the extension. Report that payment on Schedule 3, line 10 of Form 1040, Form 1040-SR, or Form 1040-NR. For Form 1040-SS filers, report it at Part I, line 9.

Joint & Separate Filing: Two Scenarios

- Separate Extensions, Joint Return

If both spouses each filed a separate Form 4868 but later file a joint return, add both payments together and enter the combined total on the appropriate line of the joint return. - Joint Extension, Separate Returns

If the spouses filed one joint Form 4868 but later file separate returns, the payment can be entered in full on either spouse’s return, or divided between them in any amounts they agree on.

Further Reading

- Form 1040: What Tax Practitioners Need to Know Before Filing Season – A comprehensive guide covering what changed on Form 1040, how the numbered schedules connect, and what to verify for every client before the return is filed.

- How to Fill Out the IRS W-4 Form Correctly (Step-by-Step) – A step-by-step walkthrough of every section of the W-4, covering withholding adjustments, multiple jobs, dependents, and the most common errors employees make.

- How to Complete Form W-2 (2026): Box-by-Box Instructions for Employers – A box-by-box breakdown of Form W-2 for the 2026 tax year, covering what goes where, what changed, and how to avoid the errors that trigger SSA processing delays.

- IRS W-9 Form: What It Is and How to Fill It Out Correctly (2026) – Covers who needs to complete a W-9, how to fill it out correctly, and what the information is used for by the business or individual requesting it.

- How to Order IRS Forms by Mail in 2026 – A practical guide to requesting physical IRS forms and publications by mail, including what is available, how to order, and what to expect on delivery.

- Free Fillable IRS Forms: What They Are and Where to Find Them in 2026 – Explains what IRS Free Fillable Forms are, how they differ from tax software, and where to access them for the 2026 filing season.

- IRS Form 8949: How to Report Capital Gains and Losses in 2026 – A practitioner-level guide to completing Form 8949, covering which box to check, how to handle broker-reported transactions, wash sales, and how the form feeds into Schedule D.

Conclusion

Filing a tax extension in the US comes down to one form: Form 4868. Filed by April 15, 2027, it removes the late filing penalty and gives you until October 15, 2027, to file a complete and accurate return.

However, any tax owed for 2026 remains due on April 15, 2027, and interest accrues from that date regardless of when the return is eventually filed.

File the extension on time, pay as much of the estimated liability as possible by the deadline, and close the return before October 15, 2027. That is the entire job the form is designed to do.

Frequently Asked Questions (FAQs)

No. The extension is automatic, provided the form is filed on time, the estimated tax liability on line 4 is reasonable, and the client is not under a court order to file by the original deadline. The IRS will contact you only if the request is denied, which is uncommon when the form is completed correctly.

Yes. US citizens and residents living and working outside the US and Puerto Rico, or serving on military or naval duty abroad, already receive an automatic two-month extension. Filing Form 4868 and checking line 8 by June 15 extends the filing deadline by a further four months, to October 15. Interest still accrues from April 15 regardless of location.

Yes. You can file Form 4868 electronically through the IRS Free File program at irs.gov/FreeFile or through an IRS-approved tax software or professional e-file system. Once submitted, you receive an electronic acknowledgment. Retain it as proof that the extension was filed on time.

You can file a free extension in two ways. First, through the IRS Free File program at irs.gov/FreeFile, which is available regardless of income level. Second, by making an electronic payment through IRS Direct Pay and selecting “Extension” as the payment reason. The IRS automatically processes the extension without requiring you to file the form separately. Either way, the extension gives you until October 15, 2027, to file your return. Any tax owed is still due April 15, 2027.

File Form 4868 by April 15, 2027. You can do this by mailing the paper form, e-filing through IRS-approved tax software or a tax professional, or making an electronic payment and selecting extension as the reason. All three routes produce the same result: an automatic six-month extension to file your return.

Taxpayers who file Form 4868 by April 15, 2027 have until October 15, 2027 to file their return without a late filing penalty. The extension covers filing only. Any tax owed must still be paid by April 15, 2027 to avoid interest and the late payment penalty.