GPT-3.5 failed the CPA exam with a 48% average score. Eighteen months later, GPT-4 scored 85.1%, including 91.5% on Auditing and Attestation.That is the number behind every “will AI take over accounting” headline this year. But passing a test and replacing a professional are not the same thing.The mistake most firms make is treating this as a talent question. It is a pricing question.

No, AI will not take over accounting. But it is already replacing the billable hours you used to charge for, and firms still charging 2022 rates for 2026 work are the ones actually at risk.

Is AI Really Taking Over Accounting Right Now?

AI is not something accounting firms are still waiting on, ready to take over accounting overnight. It is already sitting inside the tools most firms use every day, quietly finishing tasks before anyone has to ask.

Every task inside a firm splits into two kinds. One kind has a right answer once you have the data. The other kind needs someone to decide what the data means.

Is this categorization right for this client? Is this variance a real problem or just noise? Does a number that looks fine actually hide something? Those questions still need a person. Software can show the data. It can’t decide.

The first kind is already automated. A bookkeeper used to start the day matching yesterday’s bank feed to the ledger by hand. Now that happens overnight, and the transactions are already coded and matched before anyone logs in. Invoices get read and posted the same way, before a data entry clerk ever opens the file. A reconciliation that used to take an associate a full afternoon is now a five minute check of what the software already built. None of that ever needed a CPA’s judgment.

This is the work that used to fill a junior accountant’s first year on the job, and it is the first to disappear. This is what people mean when they ask whether AI will take over accounting, and for this slice of the work, it already has.

Just having the software is not the same as getting value from it. Some firms let AI code transactions, then still have a partner recheck every single one anyway. That does not save anyone time. The firms actually gaining from AI trust it with the routine work, then spend the time they save on review and advisory instead.

Which Accounting Roles Will AI Replace First?

Not every role carries the same amount of risk. Bookkeeping clerks and entry level staff are the most exposed, since so much of their week is routine work AI can already do. For everyone else, exposure depends less on job title and more on how much of the week is routine versus how much depends on judgment. That does not mean AI is going to replace accountants across the board. It means specific tasks, not job titles, decide who is exposed.

The Bureau of Labor Statistics data shows this split clearly. Bookkeeping clerks are projected to decline by 6 percent between 2024 and 2034. Accountants and auditors, on the other hand, are projected to grow by 5 percent over the same period, faster than the average across all occupations. Two closely related roles, heading in opposite directions.

| Role | Task Exposure | AI Impact Today |

|---|---|---|

| Bookkeeping clerks | Data entry, reconciliation, invoice matching | High, largely automated |

| Staff and junior accountants | Month end journal entries, bank reconciliation | High on routine tasks, human review still required |

| Tax preparers | Return drafting, data collation | Medium, AI drafts, a human still defends the position |

| Auditors | Testing, anomaly detection | Medium, sign off stays human |

| Controllers, advisory, CFO track | Strategy, client relationships, judgment calls | Low, demand rising |

The gap between those numbers is bigger than it looks on the surface. A junior accountant spending most of the week on journal entries and bank reconciliation shares more AI exposure with a bookkeeping clerk than with a controller, task for task. The job title survives. It’s just harder to get in.

Where AI Won't Take Over Accounting

The work that still requires a human is the work that carries legal and professional liability, and no software update changes that.

A CPA signs the audit opinion. A CPA represents a client before the IRS. Neither is a formatting task AI can absorb, because both carry personal professional liability that a model cannot hold.

The same boundary applies to judgment calls that depend on context AI does not have. Detecting fraud often means reading intent and business relationships, not just flagged anomalies in a ledger. Interpreting a gray area in tax law for a specific client’s facts is a defense, not a lookup.

Did you know?

GPT-4 scored 91.5% on the CPA exam’s Auditing and Attestation section. Firms still require a licensed CPA’s signature on every audit opinion regardless of that score.

What AI Can Do & What Still Needs You

The line between the two is not about how hard a task is. It is about whether the task has a single right answer or needs someone to weigh context. AI is fast and accurate on the first kind. On the second, it can prepare the work, but a person still has to make the call and carry the responsibility for it.

Here is how that split looks across the tasks that fill most of a firm’s week.

| Task | AI Can Do | Human Must Verify |

|---|---|---|

| Bank reconciliation | Match transactions, flag mismatches, build the draft | Whether a flagged mismatch is an error or a legitimate timing difference |

| Transaction coding | Categorize entries based on past patterns | Whether the category is right for this client's specific situation |

| Invoice processing | Read, extract, and post invoice data | Whether an unusual invoice signals fraud or a genuine one-off |

| Variance analysis | Draft plain language commentary on what moved | Whether a variance is noise or a real problem worth raising |

| Tax return drafting | Populate the return from source data | Whether a gray area position will hold up if challenged |

| Audit testing | Scan full populations, surface anomalies | Whether an anomaly reflects intent, and signing the opinion |

Every item is a judgment call, not a calculation. This is why AI will not take over accounting outright, it hands the routine work back done, but the decisions in that right hand column stay with you, and that is the part clients still pay for.

What the Spreadsheet Era Actually Proves About This Moment

Spreadsheets changed ledger clerk jobs in the 1980s. AI is doing the same thing to bookkeeping clerks now. The job did not disappear. It just changed.

Before spreadsheets, doing the books by hand was a paid skill. Then spreadsheet software became common, and that skill was no longer rare. Clients stopped paying extra for it. The accountants who did well next moved into analysis and advice instead, the kind of work software could not do.

AI is doing the same thing, just faster. This time, it is not ledger entries that disappear. It is reconciliations, document summaries, and first draft tax returns. Every past scare about technology ends the same way. The software never replaced accountants. It just took over one task at a time.

The lesson is the same. It is just happening faster now. Firms that wait too long will still be billing by the hour for work AI now finishes in minutes.

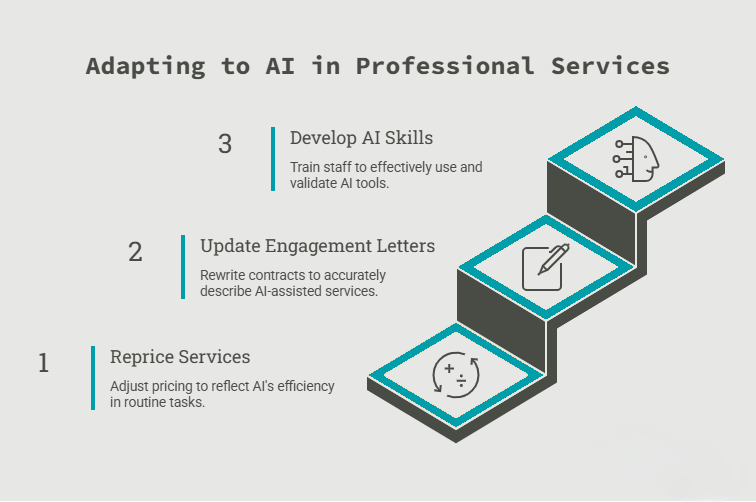

What Should a Firm Actually Change This Year?

None of this matters until it changes three things , what you bill, what the engagement letter says, and what your team can do.

Reprice the Work AI Now Does for You

Picture a bank reconciliation. An associate used to spend close to two hours matching transactions by hand, checking each one against the bank statement, and tracking down anything that did not match. AI now does that same work in a few minutes. It matches the transactions, flags the ones that look off, and leaves a clean file ready for review.

This changes what a firm can honestly charge for that work. If a task now takes minutes instead of hours, charging the old hourly rate stops making sense. The client may not understand exactly what the software did, but they notice the result. Something that used to take a few days now comes back the same afternoon, and clients start to ask why they are paying the same amount for it.

Firms that handle this well do not cut every fee across the board. Instead, they lower prices on the routine compliance work, the kind AI now handles, since that part genuinely costs the firm less time to deliver. At the same time, they raise prices on advisory work, like tax planning or financial guidance, because that part is still built entirely on a person’s judgment. That is where the real value sits now, and it is worth charging for accordingly.

Put the New Scope in Writing

Think about an engagement letter written back in 2023. It probably describes a bookkeeping service that assumes someone manually enters and reconciles transactions each month. That is not how the work gets done anymore. AI now handles most of that automatically, and the letter never says so. When a client asks why they are paying the same fee for what looks like less manual work, the firm has no clause to point to. That gap between what the letter says and what actually happens is exactly where scope creep and fee arguments start.

Fixing this means going back through every service that changed speed or method and rewriting what it actually includes, not just adjusting the price at the bottom. Doing that by hand across dozens of templates and hundreds of clients is its own slow, error prone project. Firms are handling it with tools like FigsFlow, which lets a firm rebuild a service description and its pricing logic together, in one pass, instead of retyping the same clause into every template one at a time.

Build the Skill Set Clients Will Pay For

The AICPA launched its Profession Ready Initiative in February 2026, and it names this skill gap directly. It says early career CPAs need three things most of all. Comfort using AI tools day to day. The ability to check AI generated output and catch when it is wrong. And basic data visualization skills, things like reading a chart in Power BI or Tableau. None of these are the deep technical accounting knowledge that used to define a strong junior hire.

None of that means learning to code or becoming a data scientist. It means treating a dashboard the same way accountants have always treated a general ledger, as a working document you read closely, not a screen you glance at and trust blindly. A junior accountant who can look at an AI generated variance report and immediately spot the one number that does not make sense is more valuable now than one who could build that report by hand.

Where the Advisory Premium Is Actually Heading

The fastest growing roles inside accounting did not exist five years ago, and that alone argues against a shrinking profession.

Firms are creating AI compliance officers to keep AI use ethical and audit ready, exceptions managers to handle what automated systems flag but cannot resolve, and AI audit reviewers overseeing full visibility audits instead of samples.

The CPA credential is what makes a professional eligible to fill any of those roles. AI adoption did not weaken that credential. It raised the price of holding it. None of this argues that AI will replace accountants, or that it will take over accounting outright. It argues that the value of being one just moved.

Conclusion

So, will AI take over accounting? Not the profession, no. It takes over the billable hour, then hands that time back to spend on work worth more than the hour ever was.

The firms that reprice, rewrite the engagement letter, and build the new skills this year hold onto their margin. The ones that wait will watch a competitor quote the same job for less, because that competitor’s AI already covers the part the client stopped valuing.

So before your next engagement letter goes out, read it once more. Does it describe the work you deliver today, or the work you delivered in 2023?

FAQs

AI is part of accounting’s future, not the whole of it. It already handles data entry, reconciliation, and first draft reporting, the routine work that used to fill junior roles. But the future of the profession sits in advisory work, judgment, and client trust, areas AI supports but cannot own. The accountant’s role shifts from processing numbers to interpreting them.

AI will reshape accounting by automating the routine layer and raising the value of everything above it. Reconciliations, coding, and document review move to software, while accountants spend more time on advisory, planning, and interpreting results. Firms will reprice compliance work downward and advisory work upward. New roles, like AI compliance officers and exceptions managers, will emerge around managing the technology itself.

Yes, but not by replacing accountants. Automation removes the repetitive tasks, bank feeds, invoice matching, and reconciliation, that once took hours by hand. That changes what firms can charge for compliance work and pushes value toward advisory services built on human judgment. The job title survives. What changes is the daily work inside it and the skills firms hire for.

AI is transforming accounting by taking over the paperwork layer, coding transactions, matching invoices, and drafting reconciliations overnight. This frees accountants to focus on analysis, advisory, and client relationships. It also shifts firm economics, since work that once justified billable hours now takes minutes. The firms gaining most are those redesigning their workflow and pricing around AI, not just switching the tools on.